Acomo: Quick update

H1 2023 numbers down

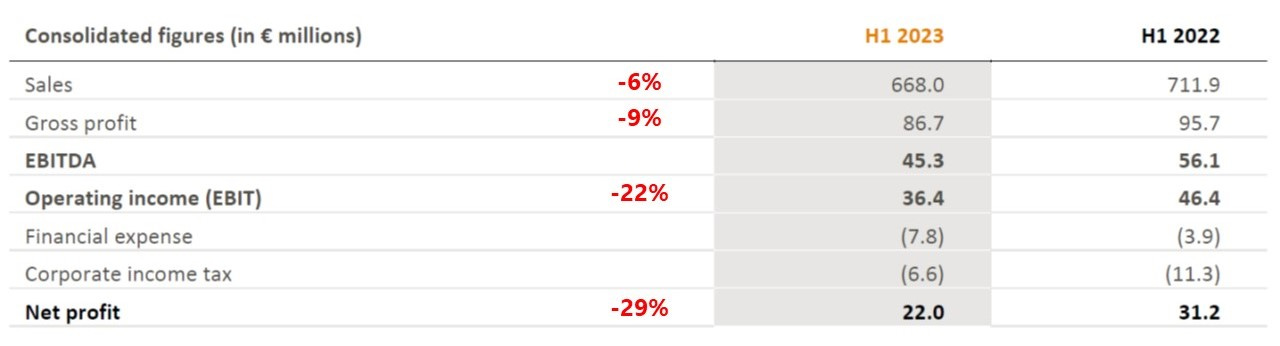

A couple of days ago Acomo published its first half results: at a quick glance, they were all negative (revenues down -6%, EBIT down -22%), and the stock has lost about 8% since. The interim dividend has also been reduced (€0.40 vs €0.45 a year ago).

But digging a little deeper, they were not a real disaster: Spice&Nuts grew EBITDA by double-digit, and E…