Bakkafrost

“Give a man a fish, and you feed him for a day

Teach a man to fish, and you feed him for a lifetime.”

P/F Bakkafrost is a best-in-class, vertically integrated salmon farmer with operations in the Faroe Islands, controlling all aspects of the value chain - from feed to finished value added products – to ensure traceability and consistent high quality.

Some quick facts

Biggest salmon farmer of the Faroe Islands, which are located about halfway between Iceland and Norway

An autonomous, self-governed territory of the Kingdom of Denmark but not in the EU: relations with the EU are governed by a Fisheries Agreement (1977) and a Free Trade Agreement (1991, revised 1998)

Part of the Danish monetary union: the Faroese krona is issued by the Danmarks Nationalbank and it's not a separate currency but rather a local issue of banknotes denominated in the Danish krone (DKK), which in turn is pegged to the euro

Bakkfrost’s annual report and financial metrics are therefore published in DKK but being listed on the Oslo Stock Exchange the share price is quoted in NOK

1. Market dynamics

Fish farming, and salmon in particular, is an industry with strong tailwinds: demand is growing but supply is somewhat struggling to keep up.

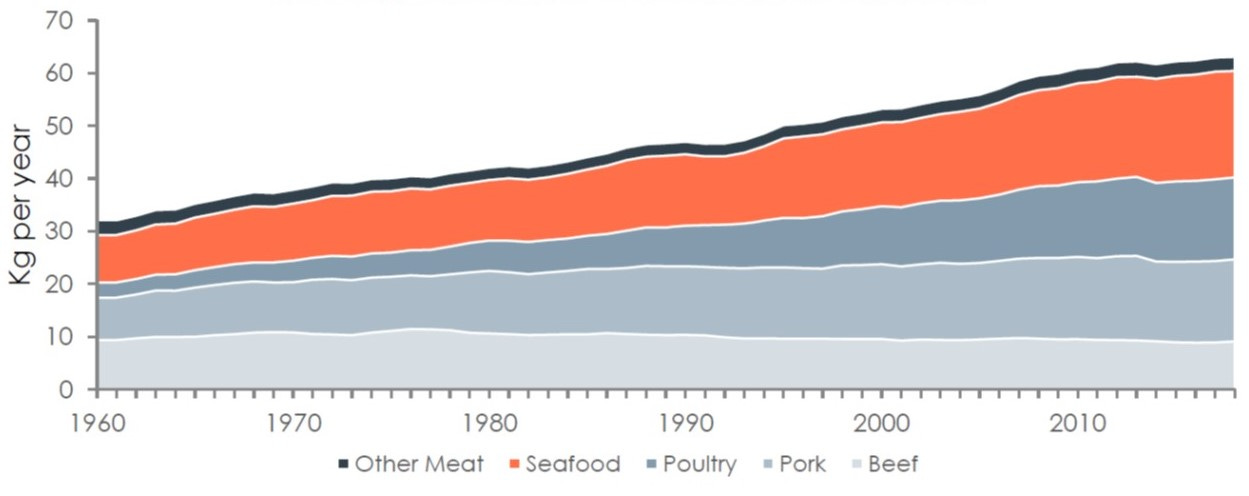

Meat as a food source has gradually become more important: global per capita consumption has more than doubled since 1960, and the seafood segment is a big contributor to this increase.

Chart 1: Global per capita meat consumption

Source: Salmon Industry Handbook 2021

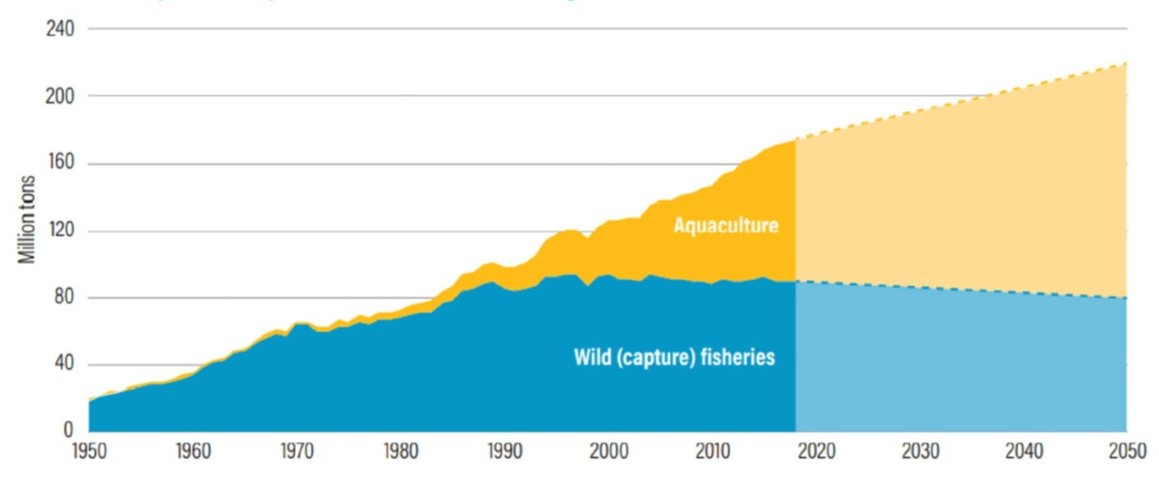

The general supply of seafood in the world is shifting more towards aquaculture as wild catch as a resource has been at capacity for years in several regions and for many important species: supply growth is today driven solely by aquaculture.

Chart 2: Aquaculture production must continue to grow to meet world fish demand

Source: Bakkafrost, historical data from FAO, projections to 2050 from World Resource Institute

Salmon constitutes a small high-end niche within the global seafood space: it’s a key category in retail due to its high nutritional value and is consistently delivered throughout the year. Farmed Atlantic salmon (sea based) has the highest level of industrialisation and the lowest level of risk compared to other aquaculture species: although relatively small in harvest volume compared to other species, it is a very visible product in many markets.

Chart 3: Considerable opportunities within aquaculture

Source: Salmon Industry Handbook 2021; the size of the circles indicates volume harvested

Demand

The global market for Atlantic salmon has increased by 7%-8% p.a. over the last 20 years on the back of several mega-trends:

Growing world population + growth in real disposable income = increased animal protein intake

Health benefits

Efficiency in terms of food to conversion ratio

Chart 4: Mega-trends drive demand

Source: Mowi

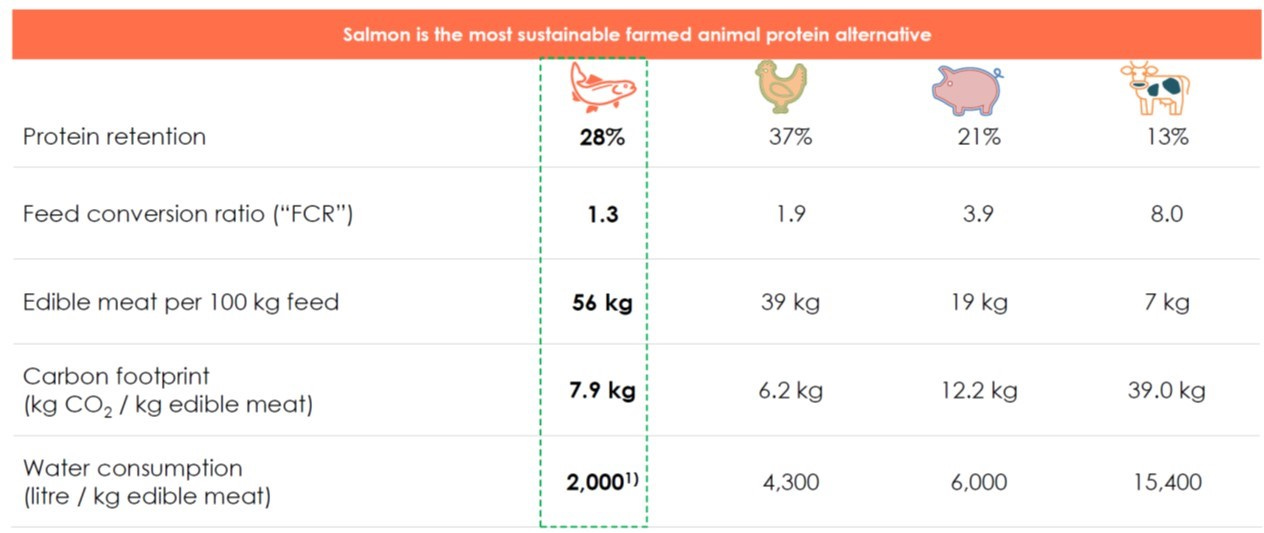

Salmon is a scientifically proven, nutritionally dense natural superfood and great for one’s health. It doesn’t hurt that it also has top appetising taste, look, texture and colour, can be prepared in different ways (raw, grilled, cooked and smoked) and is the most sustainably produced animal protein (it has the best climate footprint and top sustainability performance vs. all other animal proteins).

Chart 5: Protein Producer Index

Source: Coller FAIRR Protein Producer Index, Mowi

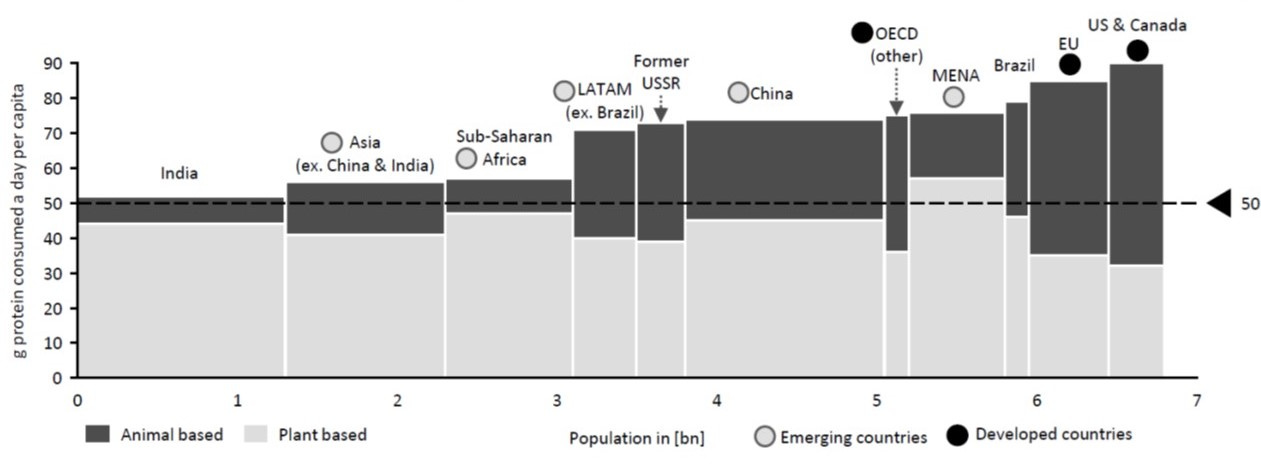

Growth in global population = increased protein consumption. The global population is growing at an unprecedent speed, resulting in an increased demand for food. As the middle class is expected to grow especially in emerging markets, this trend is likely to be followed by an increase in the consumption of high-quality proteins. Based on UN studies, it is reasonable to consider that consumption habits of emerging countries will converge with those of OECD, EU, US and Canada for the middle-class population.

Chart 6: Protein consumption in different countries

Source: World Resource Institute

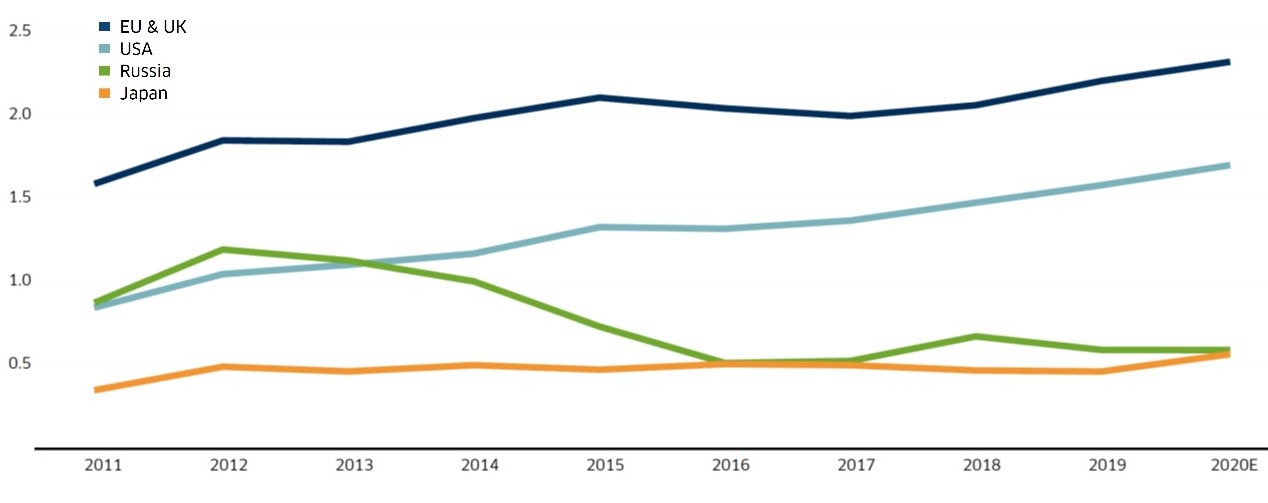

For example, despite Covid and lockdowns, in 2020 the US market for farmed Atlantic salmon grew by

~41k tonnes wfe (“whole fish equivalent”) to over 562k tonnes (+8%): with a population of 329 million, this corresponds to a per capita consumption of 1.7 kg wfe, indicating 5-6 meals per capita each year. Similarly, in the EU market (including UK), supply in 2020 increased by ~60k tonnes wfe to 1.2 million tonnes (+5%): with a combined population of 512 million, this corresponds to a per capita consumption of 2.3 kg wfe per year, or 7-8 meals per capita per year.

By contrast, the supply of Atlantic salmon to China and Hong Kong did experience a more than a 3-fold increase from 2010 to 2019 to reach 124k tonnes wfe (before crashing -33% to around 83k tonnes last year), but this translates into a per capita consumption of only 0,06 kg wfe per year.

Chart 7: Per capita consumption of Atlantic salmon (kg wfe / capita)

Source: Kontali Analyse, Bakkafrost

Within Europe, Germany, France, and the United Kingdom account for approx. 50% of total consumption, with the Nordic countries (Norway, Sweden and Finland) having the largest consumption per capita. But there is still significant growth potential among some of the largest markets, including the US.

Chart 8: Significant growth potential in all markets

Source: Kontali Analyse, Mowi

Health benefits. Salmon is rich in quality digestible proteins, omega 3 acids, vitamin D and B12, and antioxidants like iodine and selenium (source: FAO). In the light of obesity crisis, it is likely that governments around the globe will keep promoting to increase the seafood intake.

Efficiency in conversion ratio and sustainability. Salmon is the most efficient meat in production as its food conversion ratio is the lowest (i.e., the best) amongst the traditionally consumed proteins. The main reason why it converts energy and protein to body muscle and weight so efficiently is that cold-blooded animals do not spend energy maintaining body temperature like warm-blooded animals. In addition, as swimming requires less energy than walking, salmon can convert a larger share of its feed into growth than livestock can.

Finally, compared to other meat, not only seafood is better in terms of protein retention and edible yield, but it also has lower CO2 footprint and water consumption.

Chart 9: Salmon farming is a very efficient source of healthy proteins and on the right side of sustainability

Source: Salmon Industry Handbook 2021, Mowi, Bakkafrost

Supply

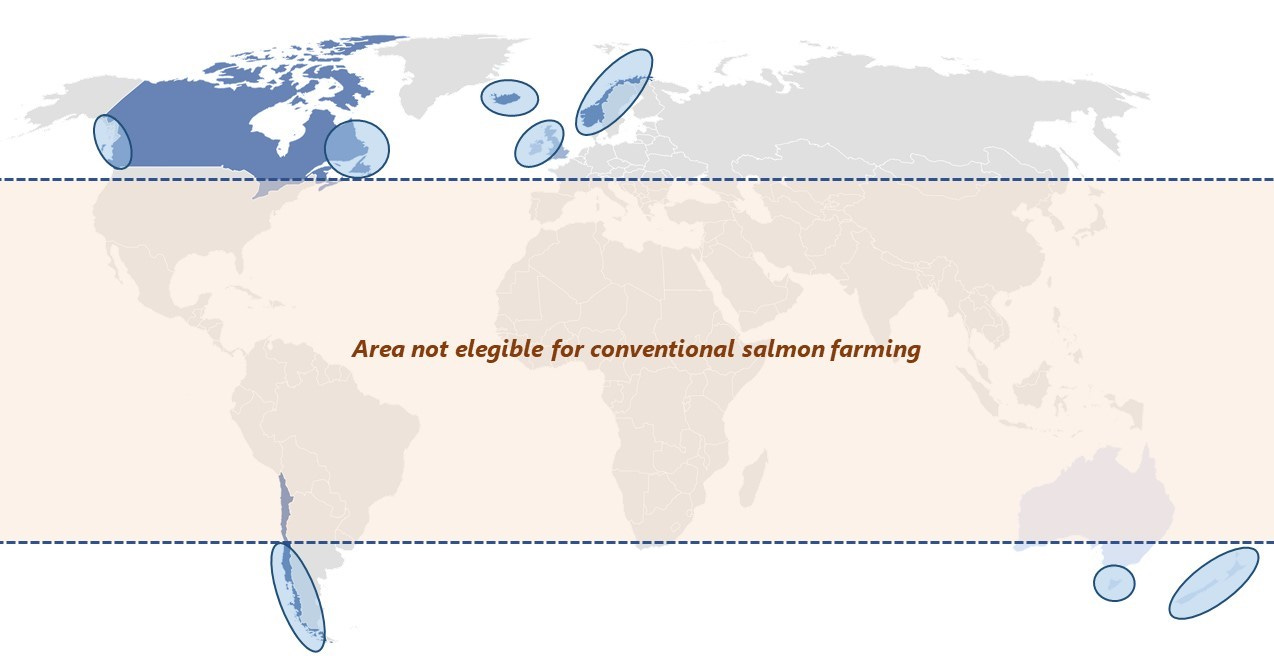

The industry is protected by technical moats because salmon farming can only be successfully implemented in areas with specific biological conditions, in particular the water temperature (the optimal is between 8 and 14 °C: freezing kills the animal, too cold curbs growth and too warm accelerates growth but increases the risk of an epidemy) and sheltered areas from the roughness of the ocean. In addition, the fish must be able to move free around the sites and there must be logistical infrastructures to supply feed, electricity, internet, manpower, etc. [Offshore farming is also an emerging approach: offshore farms are positioned in deeper and less sheltered waters, where ocean currents are stronger and therefore require more robust cages.]

The combination of these conditions is hard to find, and salmon farms are primarily located in waters protected by fjords or archipelagos around Norway, Iceland, Faroe Islands, the Northern portion of Scotland, Chile and parts of the Canadian coastline.

Chart 10: Only few regions are suitable for salmon farming

Norway and Chile provide the bulk of supply, with the Nordic country accounting last year for 50% of global harvest (1.4m tonnes wfe) and the South American country for another ~30% (780k tonnes wfe). The Faroe Islands provide around 3% of global supply.

Chart 11: Global harvest of Atlantic salmon

Source: Kontali Analyse, Bakkafrost; volume is in thousands of tonnes wfe

In addition to meteorological conditions, the supply side is also restricted by high barriers to entry that are set by local governments in all producing regions in terms of fishing licenses that restrict the maximum production. Due to environmental concerns, there is increasing pressure on governments to limit the number of licenses given out.

In Norway, for example, the number of licenses for Atlantic salmon and trout in seawater was limited to 1,087 in 2020 and it was 990 in 2011, a less than 10% cumulative growth in a decade! In addition, there has been a debate regarding new taxes: in 2020 the Norwegian government discarded a proposal to introduce a 40% resource tax and instead proposed a production fee of NOK 0.4/kg of salmon produced, which has been effective from 2021.

Norway has a higher fragmentation of the market as the government prefers decentralised structures, with 151 companies who owns commercial license for salmon and trout (total output is produced by 98 companies as some own multiple licenses through subsidiaries). On the contrary, in Chile 1,320 (300-350 in operation) commercial licenses are exploited by only 20 companies.

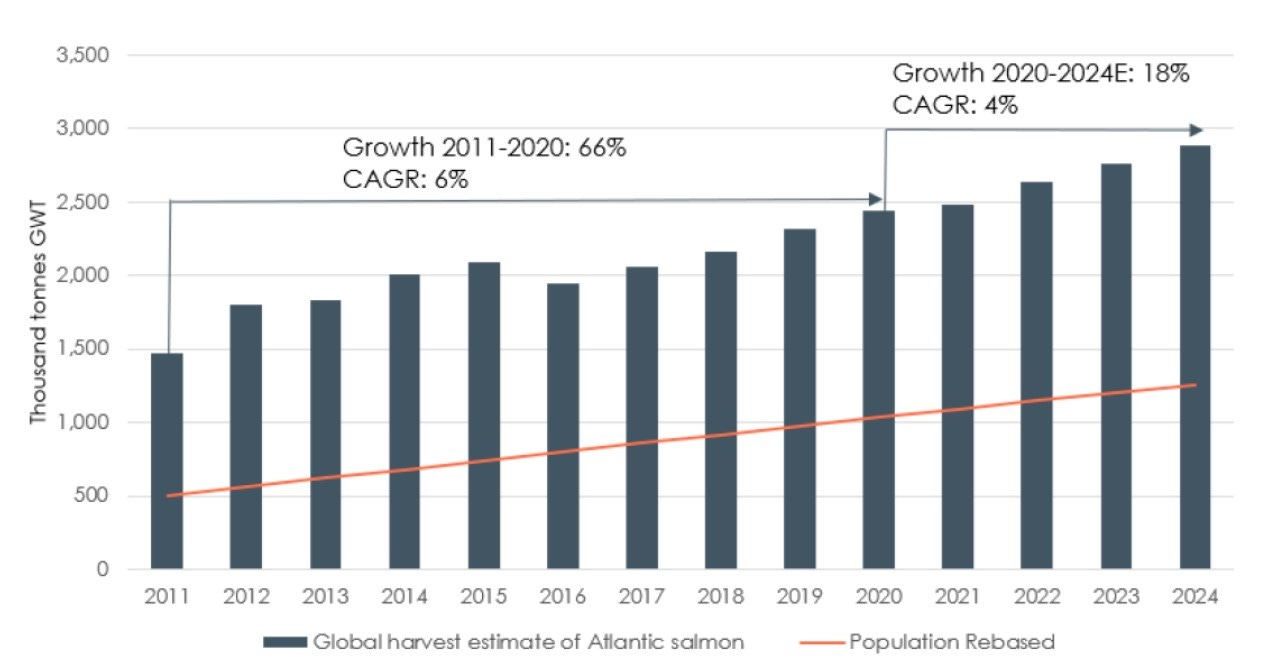

Globally, the market is struggling to catch up on the supply side with growing demand, and it is therefore expected to remain tight both in the short- and the medium-term. The background for this trend is that the industry has reached a production level where biological boundaries are being pushed: there is a limit in terms of salmon population beyond which the biomass faces diseases and exponential mortality rates. Alternative farming methods as deep offshore and land farming have insofar proven to be, respectively, inconsistent and uneconomic at scale (more on this further below).

Chart 12: Diminishing growth expectations

Source: Salmon Industry Handbook 2021

Future growth can no longer be driven only by the industry, but will rather require progress in technology, development of improved pharmaceutical products, implementation of non-pharmaceutical techniques, improved industry regulations and intercompany cooperation.

2. Production cycle: a look at capex and working capital requirements

Farming healthy, high-end quality salmons is a complicated process since it is very susceptible to infections and diseases where conditions are not perfect.

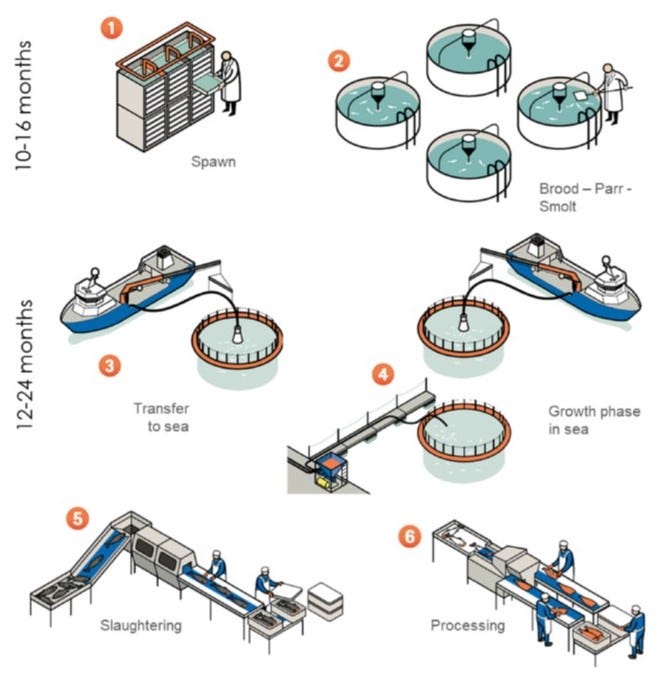

While the harvest is spread evenly throughout the year, the full production cycle takes about 2-3 years, thus making supply even more inelastic:

Hatchery (land based in freshwater tanks: 12-16 months): eggs (roe) are fertilised and fish is typically grown to approximately 100-150 grams in a controlled environment

Seawater (12-24 months, depending on water temperature and feed quality): the young fish (smolt) is released into seawater floating cages or net pens where it is grown to around 4-5kg

After harvest (2-6 months): the site is fallowed before the next generation is put to sea at the same location

Chart 13: The Atlantic salmon life/production cycle

Source: Salmon Industry Handbook 2021

There are several suppliers of eggs to the industry, so production can easily be scaled up: but the largest companies prefer to produce both the eggs and the smolts “in house”. The trend is to lengthen the time at the hatcheries to shorten the time at sea (Bakkafrost, for example, tries to grow smolts to 500g in hatcheries): this allows for higher capacity and better control of biological risks.

This long production cycle requires significant working capital in the form of biomass: investments are required for organic growth, as a larger “pipeline” of fish is needed to facilitate larger harvest volumes. And net working capital varies during the year: growth of salmon is heavily impacted by changing seawater temperatures, it grows at a higher pace during summer/autumn and more slowly during winter/spring when the water is colder. For a global operator, net working capital normally peaks around year-end and bottoms out around mid-summer.

The overall cost structure for a producer depends largely on location (not only water quality: in Norway salaries are much higher than for example in Chile, but the level of automatization is also higher) and feed prices. Feed costs are indeed the biggest single expense line (between 40% and 55% of the cost structure), with the variation due to logistics, different ingredients and different feed to conversion ratios (higher in Chile as compared to Norway, i.e. Norwegian companies get more “meat” for the same amount of feed). Other costs are for smolts (higher in UK/Scotland as there are little economies of scale), equipment (boats, transportation, processing and packaging), admin and other biological costs (i.e. mortality, an integral part of salmon farming: there are several methods to account for mortality-related expenses).

During the past decade, operating cost have been moving up: both sea lice and algae bloom caused by climate change have raised mortality issues. But it was mainly feed prices which have driven the total cost upwards: com¬modity prices for the ingredients used in the salmon feed have increased and mark-up for the feed producers have remained fairly stable.

3. Sea- vs. land-based farming

Given the limitations to grow supply, several companies have experimented with what is known as land-based RAS (re-circulating aquaculture system): producers use similar technology as conventional farming in the hatching stage, but instead of growing the last stage of life in net pens and cages in the ocean, the fish are moved to grow out tanks within the same facility.

One of the problems of the salmon industry is the location mismatch between supply and demand that creates a long supply chain that involves high freight costs. Unlike conventional farming which is far from consumers since 50% of the global harvest comes from Norway but ~50% of the demand comes from North America and Asia, land-based farming tend to be much closer to large consumer markets, with established trucking routes.

Chart 14: Global salmon supply chain

Source: Atlantic Sapphire

Land-based farming also has a wider geographic potential, with the natural environment requirements lower compared to sea-based farming: since it’s not in the ocean, it can be farmed practically anywhere (though close to low temperature ocean water is preferable due to less energy cost). Finally, there are lower regulatory barriers, as there are no limits to permits that can be issued for land-based salmon farms.

The actual technology has existed for a long period of time, but there has not been any significant player in the space until recently. While it is never a good idea to bet against technology finding a solution to practical problems, land-based salmon farming is a high-risk venture, far more so than generally appreciated, because biology is not maths.

As in many other areas of the natural resources industry, salmon farming has also experienced its fair share of the private equity boom: many fish farming projects have obtained finance, including early-stage start-ups. But land, water, licenses, facilities, working capital, filters, cooling systems, and artificial currents are expensive compared to salmon’s natural habitat (the sea), and the numbers might only add up when salmon prices are at their peak. The issue is not really number crunching, but rather the underappreciated risk of onshore farming being much slower and far less profitable than expected, especially when taking relevant mortality episodes into account.

To date, the record for land-based farming is dismal. Niri was the most prominent of the start-ups, with the largest land tank to farm salmon back in 2016. You can read the entire story here, here and here. In short, the technology was all about cleaning and recirculating water: but in 2017 the water was contaminated with detergent, forcing the plant to discontinue production and losing all the water in the process. By 2018, the “visionary” founder and CEO was gone and the plant was up for sale.

The Norwegian company Atlantic Sapphire (also a public company with Bloomberg ticker ASA NO) has been operating a 3,000-ton “commercial pilot” facility in Denmark since 2011 and has recently opened a 90,000-ton facility in Homestead, Florida, specifically to serve the large US market. The company claims to be able to reduce costs in the new plant to 36 NOK/kg vs. the 53 NOK/kg that a traditional Norwegian farmer spends in producing salmon and sending it to the US, with the savings coming almost entirely from “no-air-freight” costs (a 15 NOK/kg reduction). These projections seem to be quite optimistic: for a starter, the US is a big country, and they still have to account for logistics and distribution costs for a perishable product to distant places from Florida. And second, it’s even less clear how Atlantic Sapphire accounts for the much higher depreciation costs on a much higher initial base for the facilities: as seen in Niri’s case, the performance at the facility level is critical as the model entirely depends on it, so there is no room for interruptions or downtime, and it’s not possible to compromise on capex. Atlantic Sapphire is still loss-making despite 10+ years in operation. It is not sure whether land-based farming would ever be able to operate at scale to make it profitable.

And in a world that is ESG-obsessed, traditional farming, with its ever-rising standards, is truly the bio part of the salmon industry. In August 2018 the Danish Environment Minister announced that Denmark would put a halt to the development of fish farming at sea in a bid to protect the environment, and that the government would push for more breeding on land. But salmon production has a global environmental impact (feed, energy use, transportation, construction of production facilities, etc.) that goes beyond just environmental factors and local pollution: a report by the Norwegian Seafood Research Fund analysed the possible consequences related to shifting the total production of Atlantic salmon from traditional sea-based to land-based production and concluded that land-based production has a total carbon footprint which is 28% higher than traditional net pen production. Despite the significant reduction in carbon footprint of airfreight that a RAS system close to the end markets enjoys, from a global perspective land-based farming is LESS favourable for the environment.

Even with these (often unrealistic) assumptions, land-based farming does not seem to pose (at least yet) a threat to the sea-based companies: as at last year, land-based RAS’ share of global harvest was a mere 0,3%.

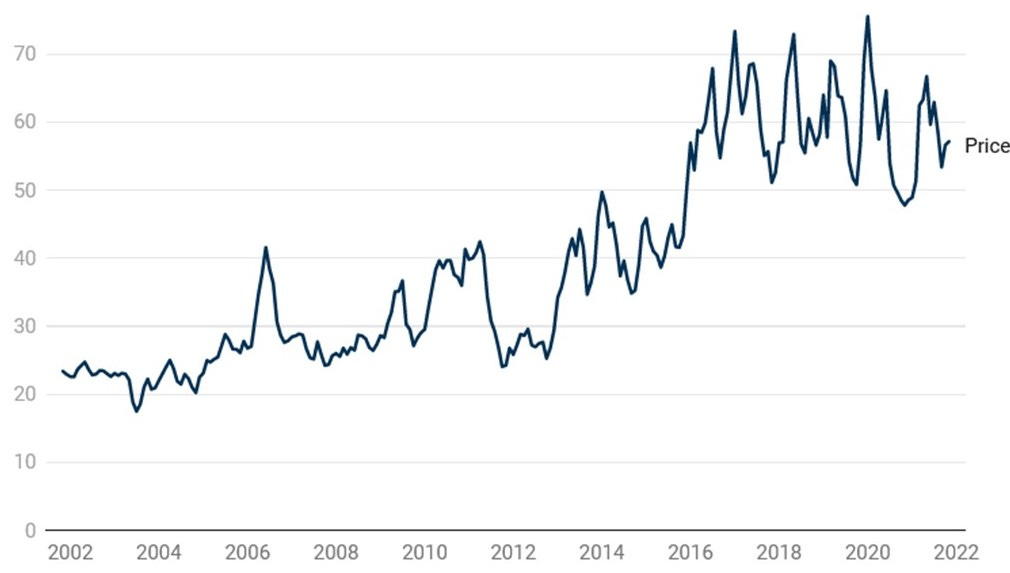

4. Salmon prices

The long production cycle, high capex and inherent risk and costs associated with production make both salmon prices and company earnings historically cyclical, and highly correlated with supply growth.

Similar to many commodity‐like businesses, salmon price has been historically highly volatile, with lower supply periods associated with higher prices. For example, after a disease (salmon anemia) destroyed much of the Chilean crop in 2010, salmon prices rose sharply but then came back in 2012.

Chart 15: Salmon monthly price (NOK/kg)

Source: Indexmundi

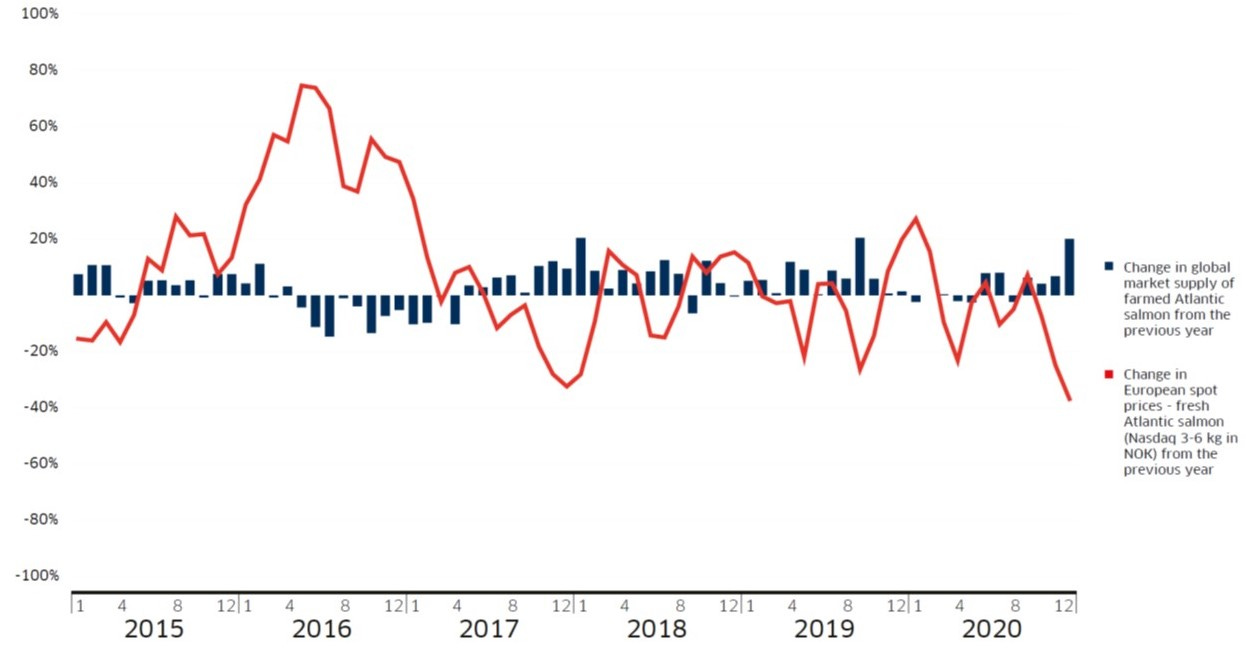

Chart 16: Supply and market prices

Source: Kontali Analyse, Bakkafrost

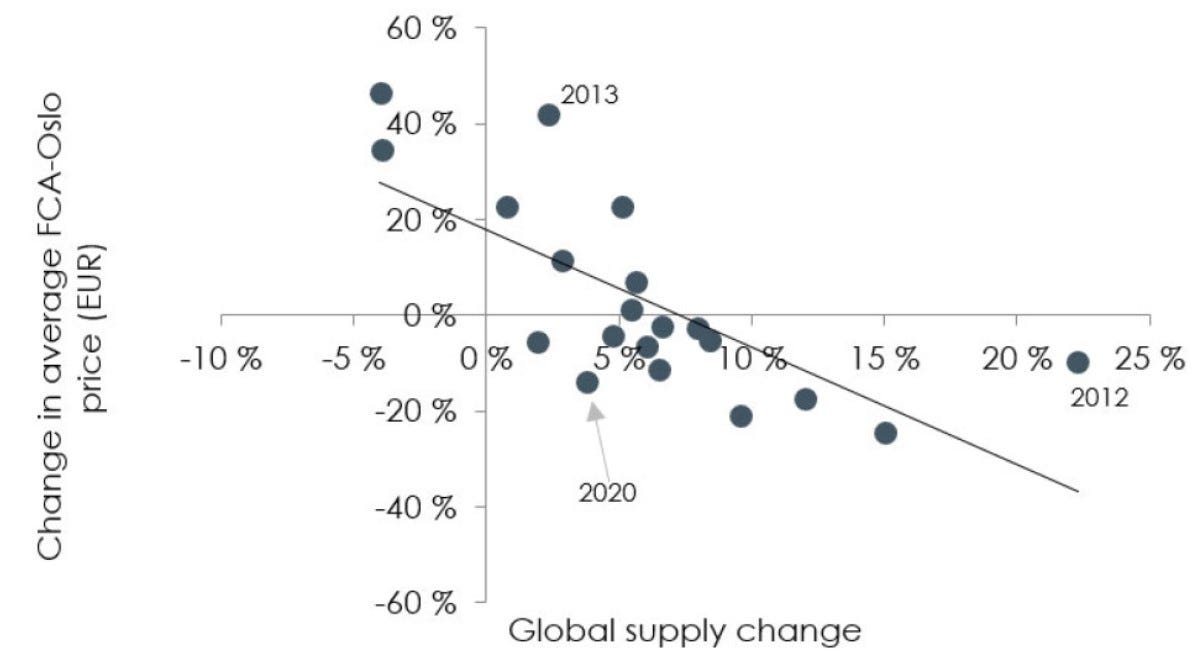

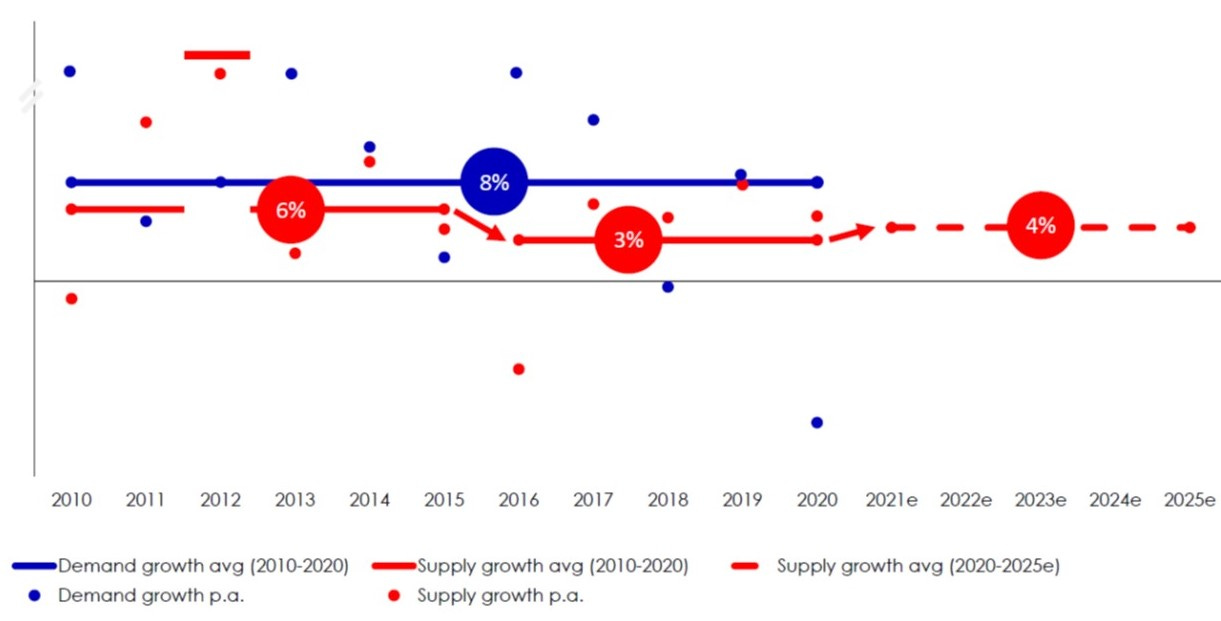

There is a strong relationship between changes in global supply and the average price, because the quantity supplied to the market is very inelastic in the short term. Salmon is perishable and marketed fresh: all production in one period must be consumed in the same period. And production levels are difficult and expensive to adjust in a three‐year production cycle. Steady demand combined with inelastic supply yields wider, more reactionary price movements: historically, a supply growth of 6%-7% has been required to be neutral on pricing.

Chart 17: Price neutral supply growth

Source: Salmon Industry Handbook 2021

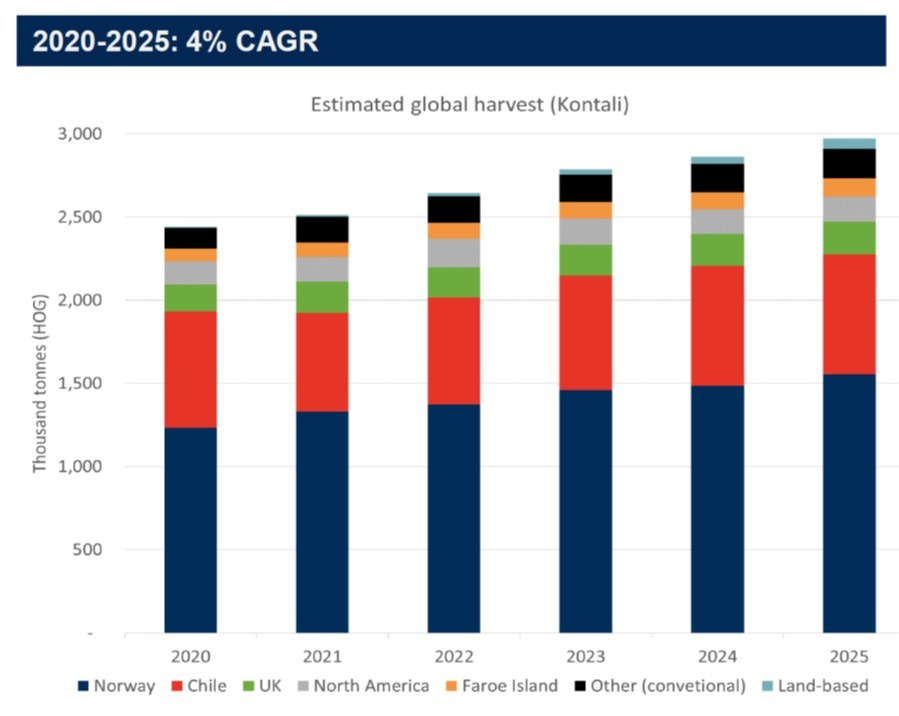

However, as discussed in the “Supply” section, forecasts for the short- to mid-term are for a more muted supply growth, around 4%: as such, demand is expected to exceed supply over the next 5 years, and in this scenario prices are expected to increase further.

Chart 18: Market outlook – limited supply

Source: Kontali Analyse, Bakkafrost

Chart 19: Demand expected to exceed supply for the next 5 years

Source: Mowi

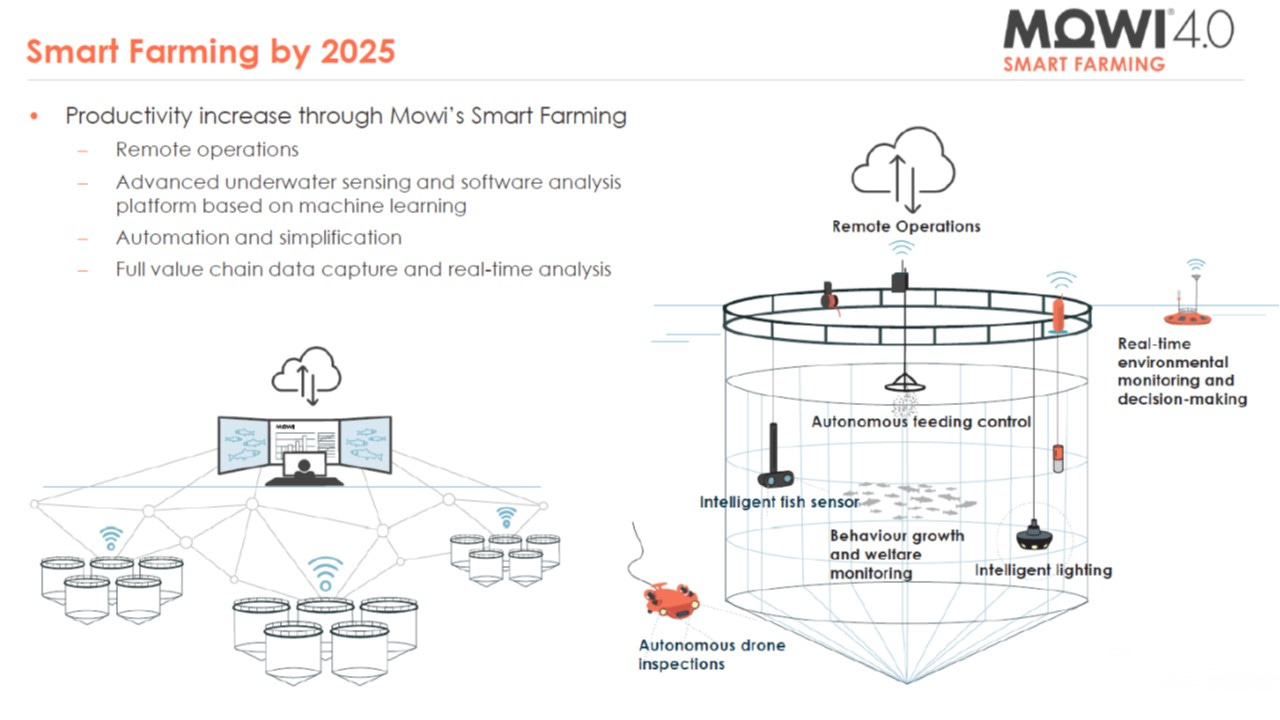

Within the industry, salmon farmers do not have really strong moats: there are no patents, network effects or other intangible advantages (brands and customer relationships have however some value). At the end of the day, it’s a commodity business without huge differentiations in quality for the end product. Going forward, R&D and technologies to optimise the farming will be even more important to provide some sort of advantage: to give you an idea of how difficult it is to grow production (and how capital-intensive sea-based salmon farming is), have a look at the solutions that Hauge Aqua, another Norwegian company, offers. (Note: if anyone is interested in VC, Hauge Aqua is indeed looking for long-term equity partners!)

Chart 20: The future of smart farming

Source: Mowi

5. A dive into Bakkafrost

Bakkafrost is a premium grade salmon producer based in the Faroe Islands. Established in 1968 by two brothers (Hans and Róland Jacobsen), in the early 2000s it grew by acquiring several smaller farming operations (both horizontal and vertical M&A) to become the largest local employer. In 2010 Bakkafrost and Vestlax Group merged and the resulting entity IPOed on the Oslo Stock Exchange.

The company owns permanent licenses in geographic locations extraordinarily suitable for salmon farming, boasts state-of-the-art production facilities as well as decades of technical know-how, and is run by a shareholder-friendly owner-manager.

Bakkafrost has adopted an integrated value chain, strengthening factors under its own control (costs and quality) and reducing reliance on third party contracts: this improves flexibility to adapt to ever changing circumstances, outweighs short term benefits from outsourcing and increases economies of scale.

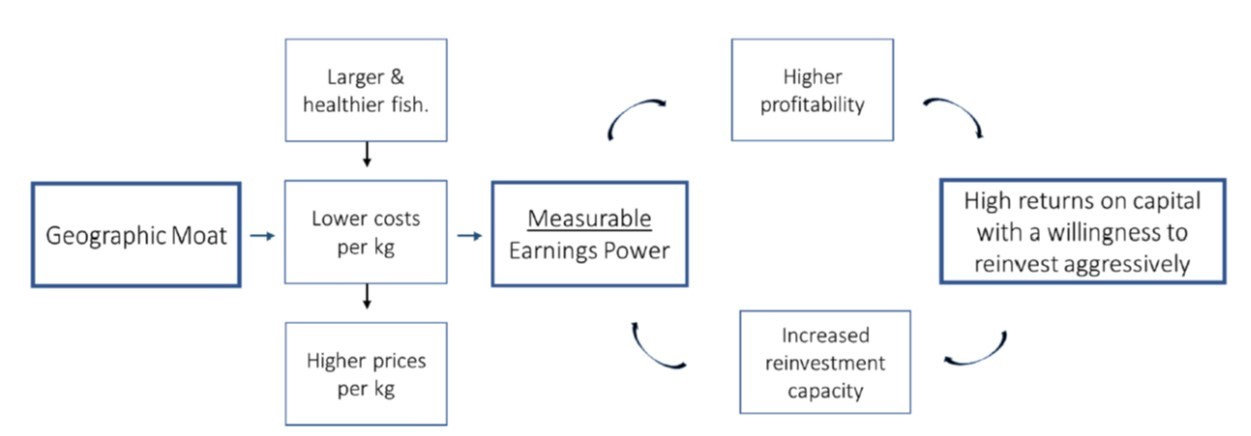

Located 200 miles north-west of Scotland, the Faroe Islands are an ideal ecosystem to farm healthy and robust North Atlantic salmons: stable water temperatures between 6-12 °C, strong currents and separation between fjords mean both lower mortality levels and lower feed to conversion ratios, which in turn translate into higher average size as there are fewer cases of early removal to harvest. Mowi, the global market leader, is also present with operations in the Faroe Islands.

The local regulations are also supportive of sustainable farming, with a long-term orientation. During 2001-2004 the islands were severely struck by ISA (infectious salmon anaemia virus) outbreaks; the response was to institute a completely revised regulatory framework (e.g.: coordinated fallowing periods, coordinated lice treatment in the direction of current, etc.) which has resulted in one of the healthiest and most predictable fish production environments in the world. Since 2006, the smolt yields in the Faroe Islands have been unmatched.

Contrary to Norway, farming licenses in the Faroe Islands come without volume restrictions: they give the right to utilise a given area of fjords for farming fish and are operated on a 12-year rolling lifespan basis with automatic renewal unless companies fail to meet basic conditions (failure to fulfil the veterinary conditions, conflict with governmental or municipalities’ planning areas, conflict with animal welfare or environmental protection, etc.).

In addition, there are restrictions on a single foreign ownership of 20% in farming companies, and one company may control a maximum of 50% of licenses (Bakkafrost has ~45% of the domestic licenses). While oligopolies are usually seen as negative for competition, this also means that the 3 key players (Bakkafrost, Mowi and Luna) are in close contact amongst themselves and with the government to implement best practices.

Finally, the Faroe Islands are an autonomous, out-of-the-radar region unlikely to confront trade restrictions: they are almost never part of recurring trade sanctions/embargos/dumping duties (e.g. Russian sanctions or the strained relationship between Norway and China when the former awarded the Nobel Peace Prize to Chinese dissident Liu Xiaobo in 2010).

Combined, these factors create a high return fish farming environment that Bakkafrost's management team has taken advantage of to create a business with a durable moat.

Bakkafrost’s revenues are derived mostly from Western Europe (67%), followed by North America (18%), Asia (8%), Eastern Europe (5%) and rest of the world (2%).

It is definitely not one of the largest companies in terms of harvested volume: including The Scottish Salmon Company (which it acquired in 2019 and is now fully consolidated), Bakkafrost has just ~3.5% of the entire salmon market.

Chart 21: Salmon farming companies by harvest volume (all farmed salmonid species)

Source: Kontali Analyse and Bakkafrost. The table include all farmed salmonids (including trout and other species), not just Atlantic salmon (which account for ~60% of harvests).

* Volumes from Scottish Seas Farms (a 50/50 JV between Salmar and Leroy Seafood) not included.

Cermaq is a fully owned subsidiary of Mitsubishi Corporation; Cooke Aquaculture and Agrosuper are private companies.

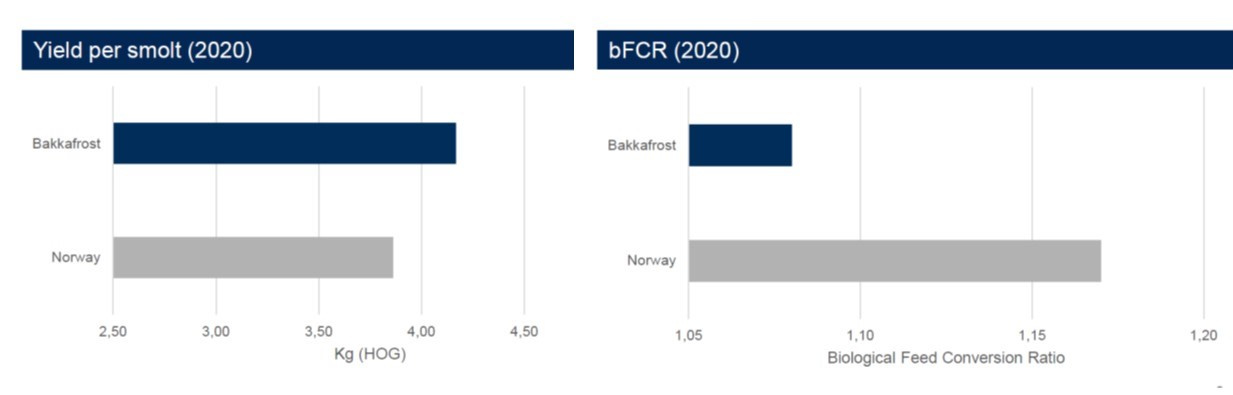

While just in the Top 10 by volume, Bakkafrost stands out as one of the most profitable salmon farming companies worldwide: it has one of the most efficient operations (yield per smolt and feed conversion ratio), the best financial margins (it’s the low-cost producer in the industry), the highest returns on capital and among the lowest risk profiles due to its low leverage. Comparatively low biological risks make the Faroese salmon farming economics the most attractive in the world in terms of predictability and unitary costs and revenues.

Chart 22: Most efficient company

Source: Kontali Analyse and Bakkafrost. HOG stands for “head on gutted”.

When it comes to operational efficiency, Bakkafrost is in a league of their own: with exception of the Covid year 2020, their business on average earns NOK20 per kg of salmon harvested, which is roughly 2x the average of any global competitor (Norwegian producers average ~NOK12 per kg harvested, Canadian producers average ~NOK10 per kg and Chilean producers have struggled to break NOK7 per kg harvested).

Chart 23: EBIT margins

Source: author’s calculations

Despite its size and wider geographical diversification, Mowi is much less efficient: size, by itself, is not a big factor on profitability (its major competitors are between 3x and 8x the size of Bakkafrost on a stand-alone basis); location is (Mowi has only around 2% of its operations in the Faroe Islands). It certainly feels like Bakkafrost is the best, most profitable company (only SalMar is on par).

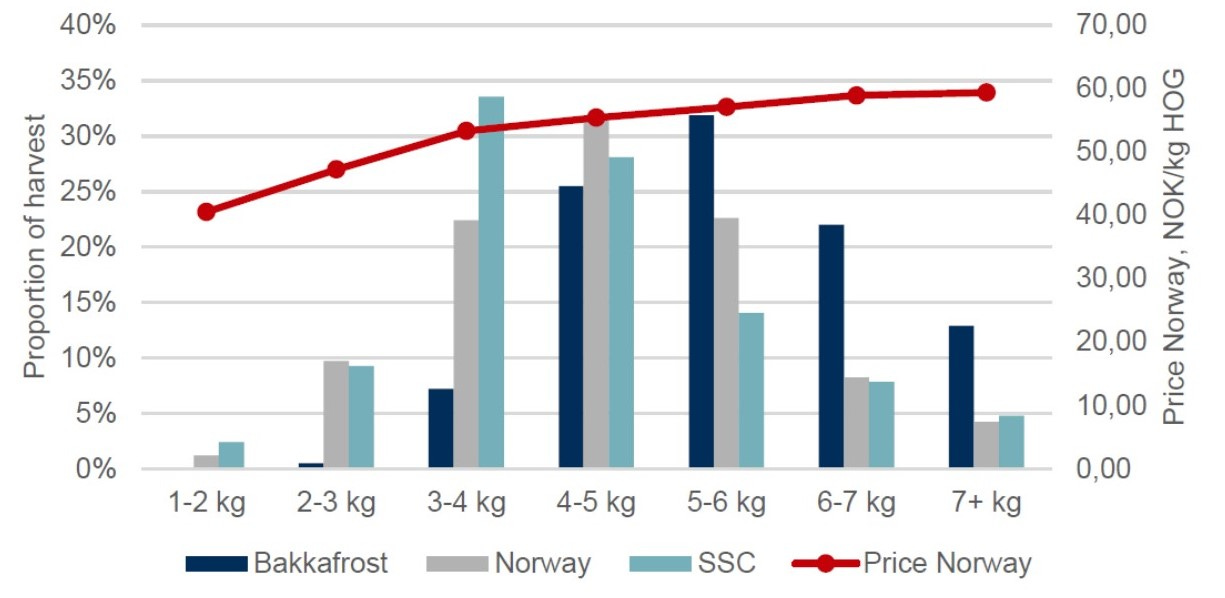

The biggest driver of this difference is indeed that salmons are sold by weight: thanks to the superior Faroese natural conditions, paired with lower losses due to mortality, Bakkafrost’s fishes are on average bigger than Norwegian salmons, which in turn leads to higher realised prices (larger salmons have historically traded at a ~5-10% premium per kg as a sign of fish health and origin). Over the last decade, Bakkafrost has consistently realized between a 15‐30% price premium over a blend of global spot prices.

Chart 24: Size distribution vs price (2020)

Source: Kontali Analyse and Bakkafrost. SSC is The Scottish Salmon Company.

Capital allocation and shareholders

Over the last decade Bakkafrost has generated an average Return on Operating Assets of 25% (the listed peer group has a market‐cap‐weighted return of around 5%, with large fluctuations according to supply performance, peaking after supply shocks and bottoming once supply is back to the market) and a FCF margin of 24% (even allowing for the drop following the acquisition of SSC, see below). Higher profitability yields more capital to reinvest at higher rates of return: a supply-constrained industry creates favourable dynamics for the consistent low-cost producers run by management with a long-term mindset.

Chart 25: The salmon “flywheel”

Source: Massif Capital

Bakkafrost’s largest shareholder (~9%) is Folketrygdfondet, the investment manager for the Government Pension Fund Norway and the largest institutional investor on the Oslo Stock Exchange (Folketrygdfondet is responsible for the domestic/Nordic investments on behalf of the Norwegian sovereign fund, while Norges Bank runs the more famous global portfolio).

However, management has a relevant stake in the company: CEO Johan Regin Jacobsen (son of the company’s founder Hans and in charge since 1989) owns ~8% and his mother another ~8%. As a successful family‐run business, Bakkafrost exemplifies many of the qualities I find attractive: an alignment of owner and manager interests, the presence of multigenerational time horizons, and the implementation of a value‐based system versus a resource‐based system.

Bakkafrost is indeed very focused on profitability and on controlling costs. The base salary for the top three managers (CEO, Managing Director and CFO) in 2019 and 2020 was in total around DKK5.3m (~$800,000), with bonuses and pension contribution accounting for another $130,000. All full-time employees receive annually 2% of their salary in bonus shares (which the company usually cover by buying back shares), but Bakkafrost has no stock option programmes running at present.

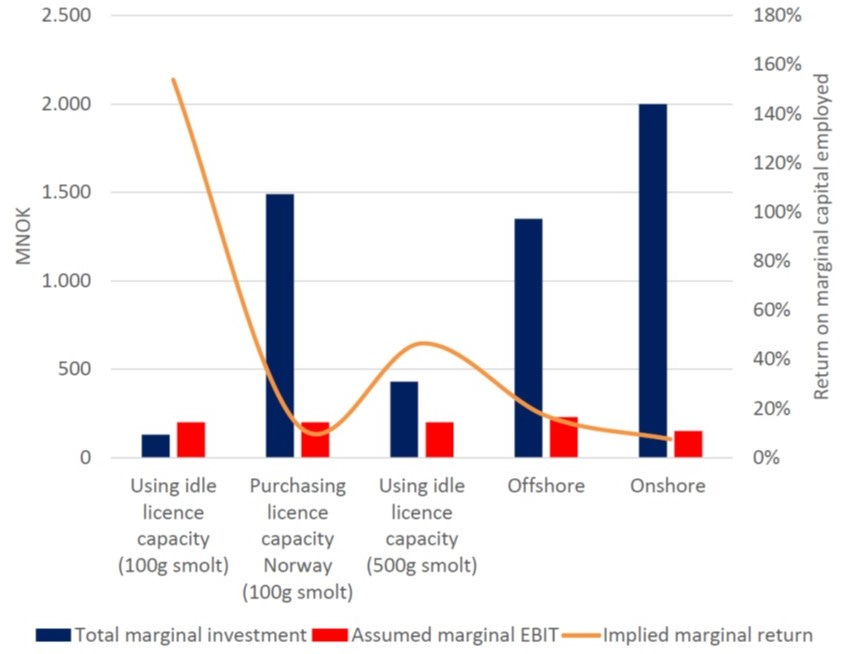

In addition, management is very conscious that capex for new, yet unproven technologies like deep offshore farming is quite high: Norwegian farmers have access to state subsidies, but that’s not the case in the Faroe Islands. As such, from the point of view of marginal returns the much better strategy is to improve the utilisation rate of current licenses, the path chosen by Bakkafrost although not fully exploited yet.

Chart 26: Illustrative example of returns

Source: Bakkafrost

Despite the M&A deals, the balance sheet is still quite conservative, currently with Net Debt / EBITDA of just 1.5x.

The acquisition of The Scottish Salmon Company (SSC)

In 2019 Bakkafrost acquired SSC, the #2 Scottish salmon farming company by harvest volumes, for the equivalent of US$440m at the time. The price paid was attractive at ~7x EBITDA, a reasonable multiple compared to both the market and Bakkafrost itself (SSC was also listed on the Oslo Stock Exchange). The acquisition was in part financed by a private placement of 15% of Bakkafrost’s share capital (5% was issued directly to Northern Link, which owned ~70% of SSC).

The strategic rationale for the acquisition included:

Access to a nice and differentiated region, characterised by high quality salmons (Scottish original provenance) priced at a premium to the market

Exposure to new end markets: roughly half of SSC’s sales were directed toward the UK, previously relatively underserved by Bakkafrost

Potential for material improvement in SSC’s profitability over a five-year horizon through realisation of identified synergies, transfer of best practices and a targeted investment programme

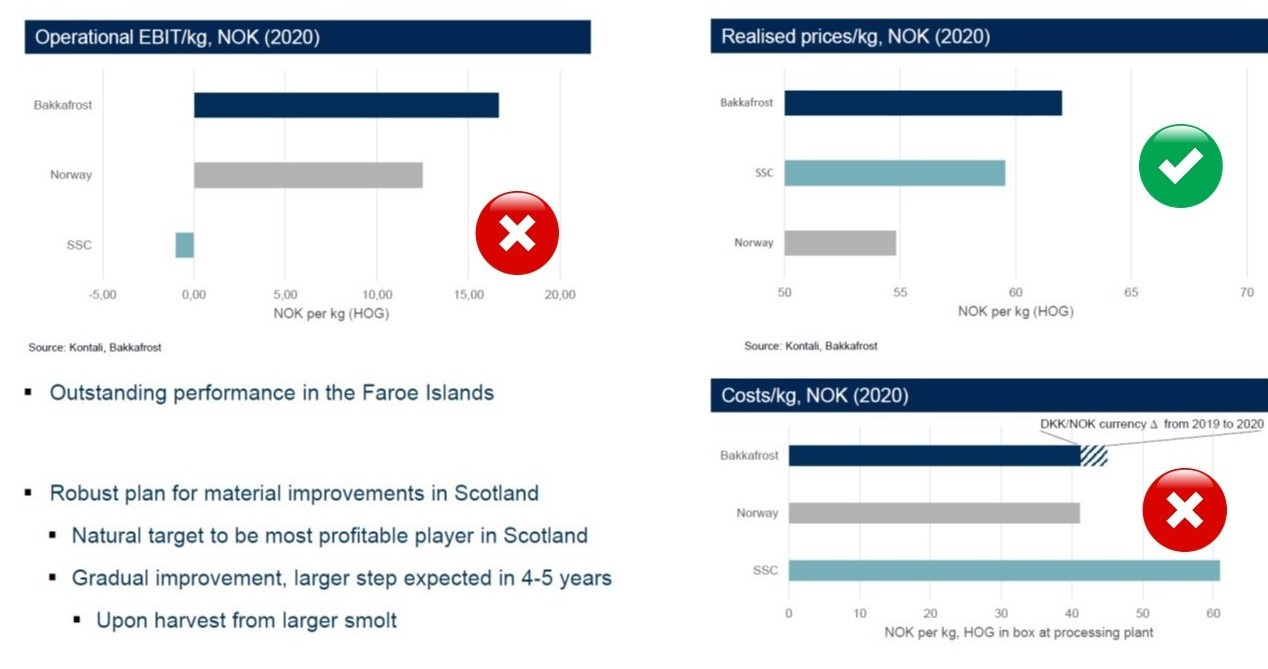

Despite the sound rational, and with the integration still underway, all of Bakkafrost’s current “issues” stem from this acquisition and the share price dropped sharply in November following the release of poor Q3 2021 results. Group revenues for the first 9 months were indeed up +16% compared to the previous year, +36% for farming in the Faroe Islands with +23% in harvest volume and an operational EBIT margin of 26% (up from 22%). But operations in Scotland were nothing short of a disaster: harvest volume was down -4% for the first 9 months (and -34% in Q3 alone) and EBIT margin was -3% (from an already paltry 2%).

In addition to some negative elements common to all farmers in Scotland (large reliance on third parties, poor zone management and limited industry co-ordination), Bakkafrost knew that when it acquired SSC it was an under-invested company (that’s why the price was low!), with obsolete seawater equipment and fragmented smolt production (low quality smolt of around <80g). The biggest issue is indeed not that SSC is not competitive on price (it is, its salmon is high quality!), but rather on the cost structure.

Chart 27: Profitability per kg comparison

Source: Kontali Analyse, Bakkafrost

That’s (hopefully) history: since the acquisition there have been many changes and massive investments to improve operations (but it will take time to see a significant improvement in margins, probably 2024).

Chart 28: Planned actions at SSC

Source: Bakkafrost

In the last 8 years Bakkafrost has invested DKK 4.1 billion (~$600m) in state-of-the-art facilities: hatcheries with advanced vaccination technology; heavy-duty and “weather-resistant” farming equipment; new FSVs and feeding systems; digitalisation for the continuous monitoring of fish welfare. Over the next 5 years (2022-2026), it plans to spend DKK 6.2 billion (over $900m) to further accelerate business transformation, with a significant portion of the capex going to Scotland.

Current valuation

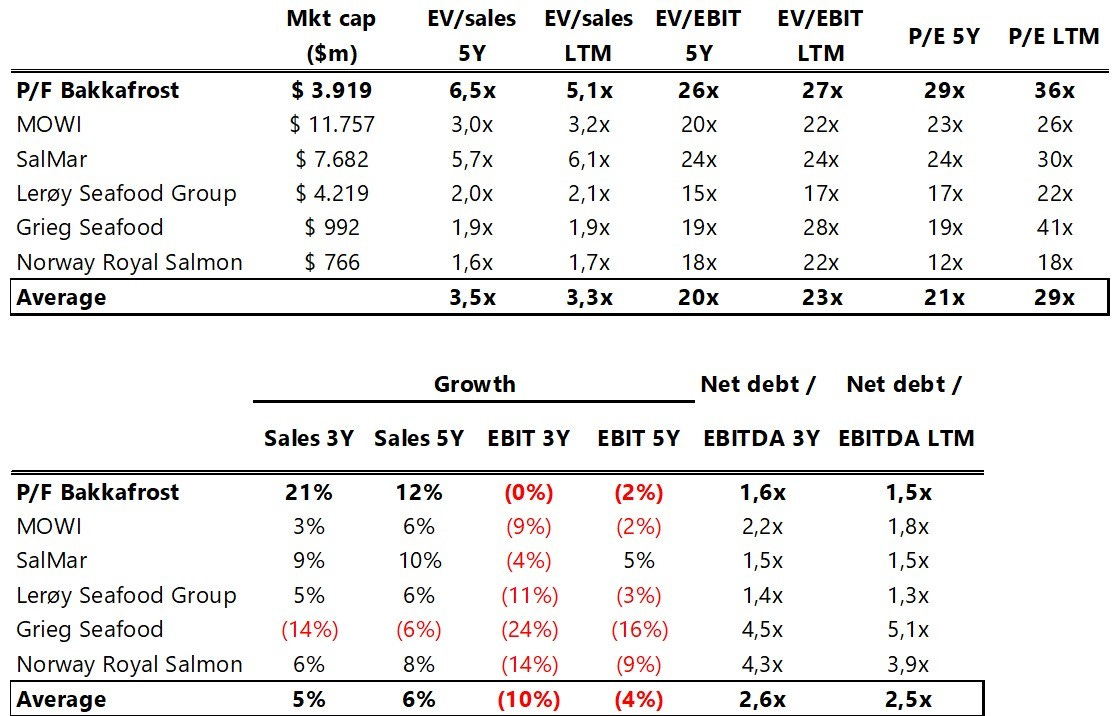

Within the industry, valuations are closely related to relative profitability per kg: it’s not surprising then that Bakkafrost is the highest valued company among its peers on several metrics, considering it also has one of the healthiest capital structures.

Chart 29: Relative valuations for listed peers

Source: author’s calculations (note: on the date of publication, Dec. 20, 2021, Bakkfrost was crashing 10%)

Bakkafrost is one of few players with large organic growth potential within the existing conventional license framework (part of current portfolio is not fully utilised), planning for over 40% conventional organic growth over the next 5 years.

Chart 30: Growth estimates

Source: Bakkafrost (in HOG ktonnes)

Risk factors

Diseases: a devastating "algae bloom" in Chile killed millions of fish in 2016, and again more than 4,200 tonnes this year. Norway has also not been immune from lices and other parasites.

Weather conditions: not just the sea quality or global warming, as in February 2020 the Faroe Islands were hit by a severe storm that lasted for several days. These are frequent and Bakkafrost has equipped itself accordingly; however, the characteristics of this storm were unusual and it caused the loss of around 1.2 million fish planned for harvest later in 2020 (an 12% reduction in expected harvest for the year).

Commodity price risk: land-based salmon farms might increase competition and drive prices down. Not really likely as today they are still too expensive to run to compete on the global stage, but not to rule out completely.

Change in consumption patterns / disruption: mostly from plant-based substitutes, with meatless burger companies rumoured to be working on something similar for fish. As for land-based salmon, these companies still have to prove their real profitability and scale: so far it has been more grandiose PR announcements than anything else.

Conclusions

Salmon farming is a poorly followed sector (Bakkafrost is covered by several banks, but mostly smallish Nordic institutions) with very attractive characteristics for investors who can determine a “fair” price for the shares and are ready to wait for it.

Among the listed companies, Bakkafrost is a best-in-class player:

Faroe Islands: ideal location for salmon farming and fewer trade restrictions

Premium products: bigger size and better quality given high-quality feed mix and geological conditions

Licenses allow for higher volumes at no extra cost: more fish in the same number of fjords (capex projects in progress)

Prudent, owner-manager with proven track record of operational excellence and high return on investment

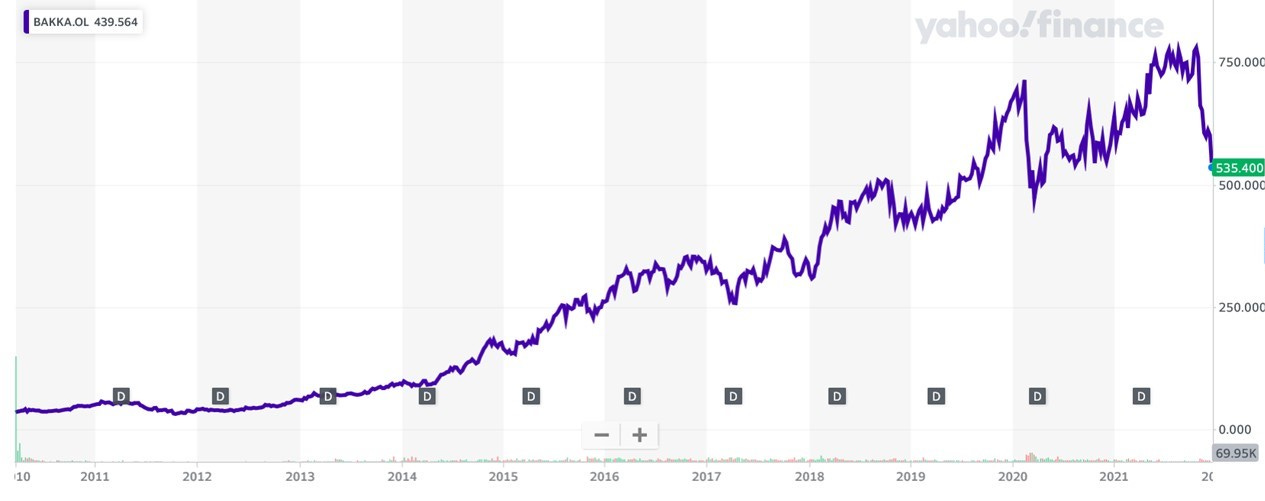

Notwithstanding the bad negative developments, Bakkafrost is a 15x bagger since its IPO in 2010.

Although the industry is very stable, the shares fluctuate a lot.

Pitched this stock at a trading competition in 2015. Pretty incredible that I have not invested more since then. I love the industry + the regulatory quirks (being technically a Danish company but accessing the Norwegian sea) make it one of my all-time favorites