Blackstone Loan Financing Limited

Attractive yield, but discount is illusory

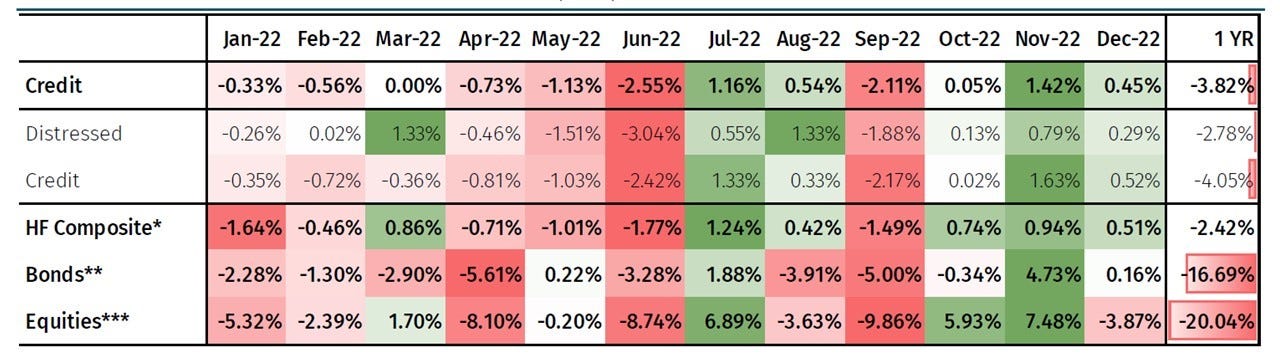

A short diversion to focus on one of the sectors that I’ve been looking into recently, listed credit funds (i.e. not the traditional investment grade or high yield ETFs): since the beginning of 2022, euro-denominated IG corporates (-14%) have indeed been hit harder than European equities (around -3%). Credit & distressed hedge funds also had a bad year.

…