doValue

“You make more money when things go from truly awful to merely bad than you do when things go from good to great.”

What is more despised these days than southern European banks? Except that, strictly speaking, doValue (DOV IM) is not a bank: it is more akin to an asset manager, earning fees from a portfolio of non-performing loans (NPLs) that it manages for third parties.

Formerly known as doBank, with around €150 billion in assets under management DOV is the leading provider of non-performing asset services (loans and real estate) in southern Europe. Since the completion of the corporate reorganisation in June 2019, doValue is no longer a banking group: the banking licence has been withdrawn (hence also the name change) and today it is authorised by the Bank of Italy as a hybrid financial intermediary. Even the presentation of its balance sheet and income statement has moved from that required for banks to the format typical of service companies.

History

With its origins going back to 1994 as Mediovenezie Banca, doValue was officially established as doBank in 2015 following the acquisition of UCCMB - Unicredit Credit Management Bank by funds affiliated to Fortress. In 2016 doBank acquired 100% of Italfondiario, one of the main operators in Italy in the field of outsourced management of performing and non-performing loans, where Fortress was a shareholder since 2000. The new merged company then listed on the Italian Stock Exchange in 2017.

Its growth path is characterised by the combination of organic development and M&A transactions that have accelerated its geographical and product diversification. In June 2019 it acquired 85% of Altamira Asset Management (with Santander remaining as a 15% minority shareholder), a leading servicer of non-performing loans and real estate assets with a presence in Spain, Portugal, Cyprus and Greece.

And in 2020 it completed the acquisition of 80% of Eurobank Financial Planning Services (FPS) from Eurobank Ergasias, a servicing company operating in the Greek market with a portfolio of around €27 billion. The agreement also included the exclusive management of future flows from Early Arrears and NPEs originated by Eu¬robank in Greece for a period of 10 years, thus consolidating doValue’s role as the strategic long-term partner of a systemic bank.

Source: doValue’s corporate presentation as at November 2021.

Via its acquisition of Fortress in 2017, today Softbank Group is DOV’s controlling shareholder with a 28% stake; another 14% is owned by Bain Capital Credit / Sankaty European Investments, with asset managers Jupiter (6.5%) and Global Alpha Capital (5.1%) rounding up the list.

Business segments

doValue operations are focused on the provision of integrated services through the entire loan life¬cycle:

NPL servicing: the administration, management and recovery of loans – both in court and out-of-court - for and on behalf of third parties.

Real estate servicing: the management of real estate assets, including the sale of the collateral originally used to secure the loans, with the aim of maximising profitability

UTP servicing: administration and restructuring of loans classified as unlikely-to-pay with the aim of promoting their transition back to a performing status (mainly carried out by the Italfondiario and doValue Greece subsidiaries)

Early arrears and performing loans servicing: the management of performing loans or loans outstanding for less than 90 days, not yet classified as non-performing, with the aim of supporting the creditor

Ancillary data and products: collection, processing and provision of commercial, real estate and legal information (through the doData subsidiary) relating to debtors as well as the provision of other services linked to the recovery of loans

Source: doValue’s corporate presentation as at November 2021.

doValue is characterized by a “pure”, independent servicer business model, open to all banks and specialised investors in the sector, which is also asset-light:

it does not require direct investments in loan portfolios or real estate assets and bears very little direct balance sheet risk. What the company offers is its IT infrastructure developed in over 20 years of experience: this wealth of data makes it possible to optimise the credit management process, improving predictive skills and the ability to anticipate market trends.

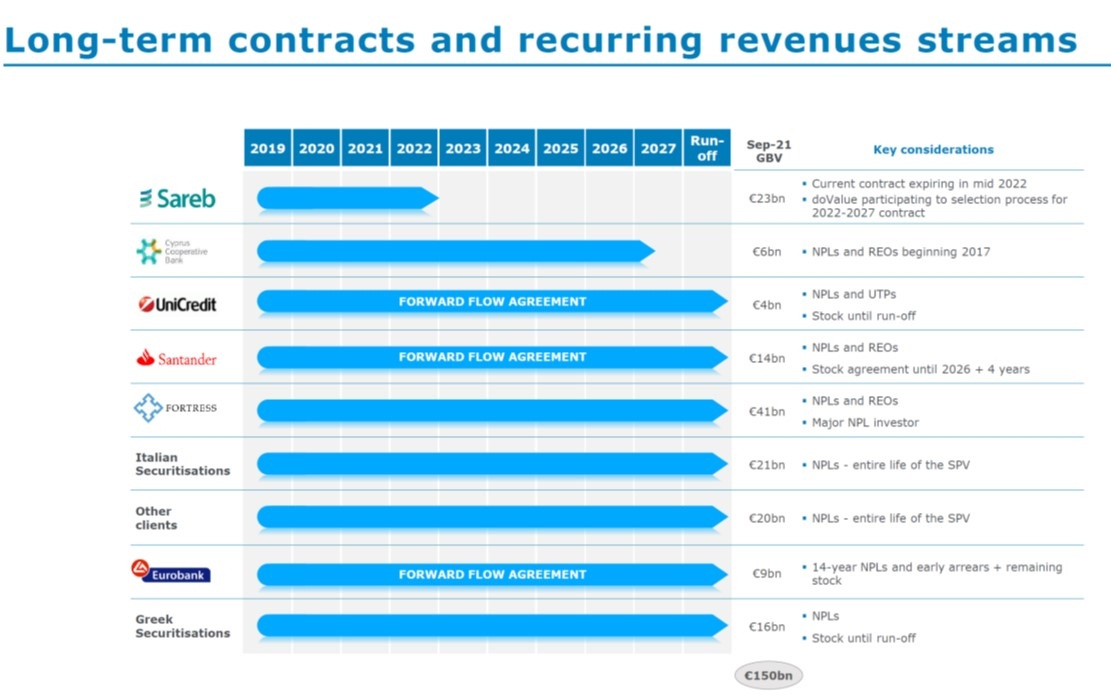

The revenue model is very simple: DOV is remunerated through long-term agreements (which provide for a recurring revenue stream) based on a commission structure that requires, on the one hand, a fixed fee established in relation to the managed assets and, on the other, a variable commission linked to the performance of servicing activities, such as collections from NPL receivables or the sale of customers’ real estate assets. Conditions for long-term contracts are decided at onset, thus giving high visibility on future revenues and earnings.

Source: doValue’s corporate presentation as at November 2021.

The reference market

Unlike natural gas, something that is never in short supply in southern Europe is the offer of non-performing assets…

Forced to hold increasing regulatory capital, most banking groups continue to pursue significant asset quality improvement plans to optimise their direct exposure: today they have transformed more and more into “financial supermarkets” selling insurance and investment products, with the concession of “credit” transferred to specialised funds and NPE asset managers. The trend over the last few years is clear: banks and funds make increasing use of operators specialised in the servicing of loans and real estate assets for activities throughout the assets value chain (starting with UTPs), a guarantee of continuous opportunities of development for DOV.

Despite the numerous sales made by banks, the stock of non-performing loans in Europe still represents a significant reference market for servicers. In particular, there is a significant concentration of these types of assets in southern Europe, a market characterized by higher-than-average NPL ratios and greater urgency on the part of financial institutions to transfer loan portfolios or promote their more efficient management. These markets are also characterised by greater management complexity, a factor that makes servicer activities even more essential.

Today doValue holds a leading market position in markets characterised by significant growth opportunities.

Source: doValue’s corporate presentation as at November 2021.

In particular, in its “home” market doValue is the clear leader with double the AuM of its main competitors, a position further strengthened with the servicing of securitisations backed by state guarantees (“GACS”).

Portfolio under management

As at September 2021, DOV managed €160.3 bn (Gross Book Value – GBV), including a €10 bn mandate secured but not yet onboarded. This is almost double the amount in 2018 thanks to the acquisition of Altamira, FPS and the mandate signed with Alpha Bank.

Source: doValue’s corporate presentation as at November 2021.

The charts below detail the composition of the managed portfolio in terms of geographical diversification, type of asset and main customers. Overall, doValue is focused on bank corporate loans of me¬dium-large size and a high proportion of real estate collateral (~75% first lien secured).

Source: doValue’s corporate presentation as at November 2021.

DOV core business requires the full functioning of public utility services, including the courts and those supporting real estate transactions. The interruption of these services in 2020-2021 as a result of the pandemic containment measures limited the operating capacities of many companies, with a predictable impact on collections and the development of revenues. Nonetheless, doValue managed to maintain a decent profitability and a solid financial position throughout the lockdown periods.

And 2021 (at least the first 9 months) turned out to be a solid year, with gross revenues increasing +37%, thanks also to the larger consolidation perimeter with doValue Greece (pro-forma, revenues still grew by +13%). Supported by the existing backbook, collections picked-up steam, but it’s the base fee component that provide the most stable and recurring revenues (kind of management fees vs performance fees for an asset manager): base fees are significantly up from historical levels (~35% of total revenues today vs 25% in 2017-2020). This is because while base fees are around 4-5 bps in Italy, they are generally higher (10-15 bps) in Spain and Greece.

Source: doValue’s corporate presentation as at November 2021.

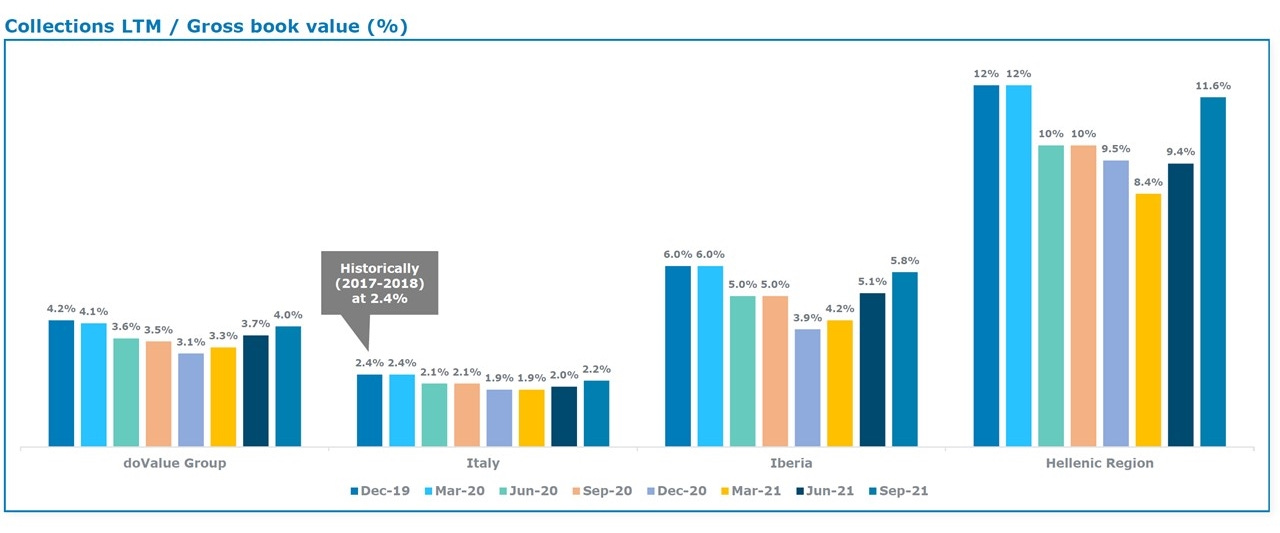

Collection rates have also stabilised following the early Covid dip and are already back to the 2019 levels. Collections are lower in Italy given the entrenched difficulties and long bureaucratic process to foreclose and repossess on collateral.

Source: doValue’s corporate presentation as at November 2021.

Current “projects”

The servicing market continues to be particularly dynamic, with banks that have been preparing for the expected increases in default rates following the pandemic and the expiration of government support measures: in 2020 doValue managed to secure new mandates for more than €13 billion, and €14 billion in 9M 2021.

Source: doValue’s corporate presentation as at November 2021.

“Project Frontier” is a new, landmark mandate (€6bn in additional GBV): the first securitisation under the Hellenic Asset Protection Scheme – HAPS by the National Bank of Greece (which is not the domestic central bank!) awarded through a competitive process. Under the structure of the deal, NBG retains 100% of the senior notes and 5% of the mezzanine and junior notes, while Bain Capital and Fortress purchases 95% of the mezzanine and junior notes. doValue Greece will undertake the servicing of the portfolio and retain some upside on the mezzanine and junior notes. The price paid for the servicing contract by doValue is c.€35m, and it will contribute approximately €5m of EBITDA per annum on average for the first 10 years (after the 10th year and until run-off estimated total EBITDA of approx. €30m).

This is a strategic deal for doValue: not only it strengthens it #1 servicer position in the country, but it is also potentially the first of a series of securitisation by NBG, the only major bank in Greece that has not sold its credit servicing operations. That said, the market didn’t like the deal at all: the stock price dropped 20% following the publication of the its details at the end of October.

Similarly, “Project Mexico” demonstrated DOV’s ability to manage complex transactions and to offer structured solutions to strategic clients: in July 2021 it submitted an offer to acquire a €3.2bn portfolio being securitised by Eurobank (aimed at retaining the management of the portfolio and with the reduction in future fees compensated by an upfront indemnity fee) and then reached a binding agreement with institutional investor for the sale of 90% of the notes, to be completed before year end. The strategic benefit of the transaction is to receive the fixed coupon remuneration plus control over servicing performance.

Last year also saw two additional, smaller acquisitions. In May 2021 it invested €1.5m for a 10% stake in QueroQuitar, a Brazilian fintech company that developed a marketplace for the negotiation of small ticket unsecured debt. The platform aims to eliminate conflicts between creditors, debtors and collection agencies (thus preserving a good relationship between the banks and its customers) with a 100% digital process, available 24/7 without human intervention.

It also invested €10 million in BidX1 (for a 15% stake), an Irish company founded in 2011 and specialised in online real estate auctions. Its platform not only allows for a transparent and efficient sale process and reduce transaction times by increasing the pool of potential buyers internationally, but it also collect a treasure of data analytics on buyers behaviours and liquidity: it has transacted over 10.000 properties for €2.5bn in value. BidX1 add a new real estate/data segment to DOV business to further support the NPL and REO activities.

Valuation

Life as a public company hasn’t been so far a success: listed in June 2017 at €9, the stock price fluctuated between €10 and €14 for a couple of years before crashing -60% in March 2020 as the pandemic started spreading across Europe. It quickly recovered the €10 level, but today the price is again around €8 - €8.50.

doValue has always maintained a solid and “liquid” balance sheet, with €140m in cash as at Sept. 2021 vs. total debt of ~€575m for a net debt position of ~€435m and 2.6x net debt / EBITDA leverage. Over the last couple of years, it has replaced the senior secured bridge facilities incurred for the acquisitions of Altamira and FPS (which carried an amortising repayment schedule) with two bonds issued in August 2020 and July 2021, thus improving the liquidity profile (bullet maturities at a later date). The newest bond (€300m, coupon 3.375%, maturity in 2026, issue price 100, current rating BB/stable from S&P and Fitch) was issued on much better terms than the previous one (€265m, coupon 5%, maturity in 2025 and issue price ~99).

Source: doValue’s corporate presentation as at November 2021.

While still in the first innings, management proved to be good capital allocators with the two big acquisitions: they both diversified the asset base and added countries with higher fixed base fees. Altamira, in particular, has been underappreciated by the market, having been completed at just above 4x EV/EBITDA: the “bigger” doValue today trades at ~6x EV/EBITDA on 2021e numbers. Management reiterated the intention to use FCFs to keep de-leveraging with the target to remain below the 2x level in the medium term, but do not rule out the possibility to capitalise on future M&A opportunities for market consolidation and expansion in contiguous higher growth sectors. For the right transaction they would feel comfortable in raising debt up to 3x EBITDA.

Contrary to what is common today, DOV has a very “simple” accounting presentation with few adjustments: there are some “non-recurring items” (for example in Q3 2021 there was a payment of €33m for a tax claim related to an inspection by Spanish authorities into Altamira’s 2014 and 2015 accounts) and no need for fx hedging as 100% of current business is in euro. The limited capex needs - mostly related to IT - imply a strong cash flow conversion from EBITDA.

If you look at doValue like at a bank, it’s not “dirty cheap”: current P/BV is 1.6x and P/E is 37x. But these metrics don’t the whole story: P/BV is not outlandish for a company that before the pandemic was steadily generating a ROE above 20% (30% in 2019 and estimated at 14% for 2021 even including non-recurring items), and normalising margins to the pre-pandemic and excluding the non-recurring tax claim the P/E drops to 16x on an unlevered basis.

Another way to look at valuation is by using assets under management. When it was listed in 2017 doValue stood at 1.20% EV/AuM; two years later, despite the growth in GBV, it traded at 0.75% EV/AuM (in part explaining the sideway price movement). Altamira was also bought for 0.75%, while FPS cost 0.90%. Today, the bigger doValue still trades for 0.75% EV/AuM, despite being more diversified and having a better base fee composition: the revenues/GBV ratio is today above 30 bps vs. ~20 bps when it first listed.

Following the indications of the Italian government, the company elected not to pay a dividend in 2020. With the current policy (a minimum payout of 65% of reported net income), the proposal for 2021 is for €0.50, implying a ~6% dividend yield at current prices.

Risks

Recession: the most obvious risk in the short- to medium-term is a prolonged recession caused by the corona virus: borrowers are already finding servicing their loans more and more difficult, and governments’ moratoriums have mostly been lifted

Political risk: never a risk to underestimate in southern Europe, and Italy in particular: while the leadership of Mario Draghi has greatly helped over the last 12 months (the BTP-Bund spread has halved vs. few years ago), some more radical reforms are still needed, and it’s not clear the current coalition would be able to carry them on. Draghi might also “move up” from Prime Minister to become Italy’s president in the next few days, which likely means new elections to be called soon.

Integration of Altamira, which is more focused on REO than the traditional NPL servicing.

Competition: while the level of competition for managing big NPL portfolios remains pretty low (few servicers are able to on-board massive numbers of files in a short period), it is higher for smaller tickets, with Tier 2 competitors becoming more aggressive on prices in order to gain market share (last year doValue declined to participate in several “auctions”).

M&A: with the current economic conditions benefitting larger players (as smaller servicers lack geographical and asset type diversification), doValue might be tempted to further increase its market share and managed assets via targeted M&A transactions. But these actions could actually “diworsify” DOV’s risk profile, rather than improve it

Share overhang: despite being a very small position within Softbank’s investments, there have been speculations and rumours that the Japanese investor might be willing to dispose of its stake.

Conclusions

The trend in asset disposal by large banks is a significant tailwind for doValue, and the decision to abandon the banking structure brought further benefits:

1) the ability to deploy balance sheet for accretive M&A

2) lower regulatory costs (including not being thoroughly scrutinised by the ECB for acquisitions)

3) a better alignment of corporate perception to the servicing business.

Looking forward, the on-going crisis may even present an opportunity, as the economic slowdown should inevitably lead to more loans becoming non-performing.

In my opinion, the weakness in the share price has more to do with technical issues and sentiment (potential overhang from Softbank selling; generic fear of Italian / southern European financials; …) than with its stand-alone investment merits (a declining business; poor capital allocation choices; mediocre ROE/ROIC; …)

PS: For those interested in the ESG angle, MSCI recently upgraded the company from A to AA.

I know the sector very well and I would stay clear of it. They enjoyed 10+ of giant headwinds and couldn't deliver as expected. What is also true is that DoValue is much older and established than the other players and can be a consolidator in a moment of market stress (cutting good deals). If there'll be a last-man standing in the NPL market in Europe, probably DoValue can be the one. Industry dynamics are quite bad though: the next crisis would be different from the GFC (won't be driven by RE and mortgages); it is far from sure that NPL servicer will be able to prosper from it