Grupo Catalana Occidente

A hidden insurance gem

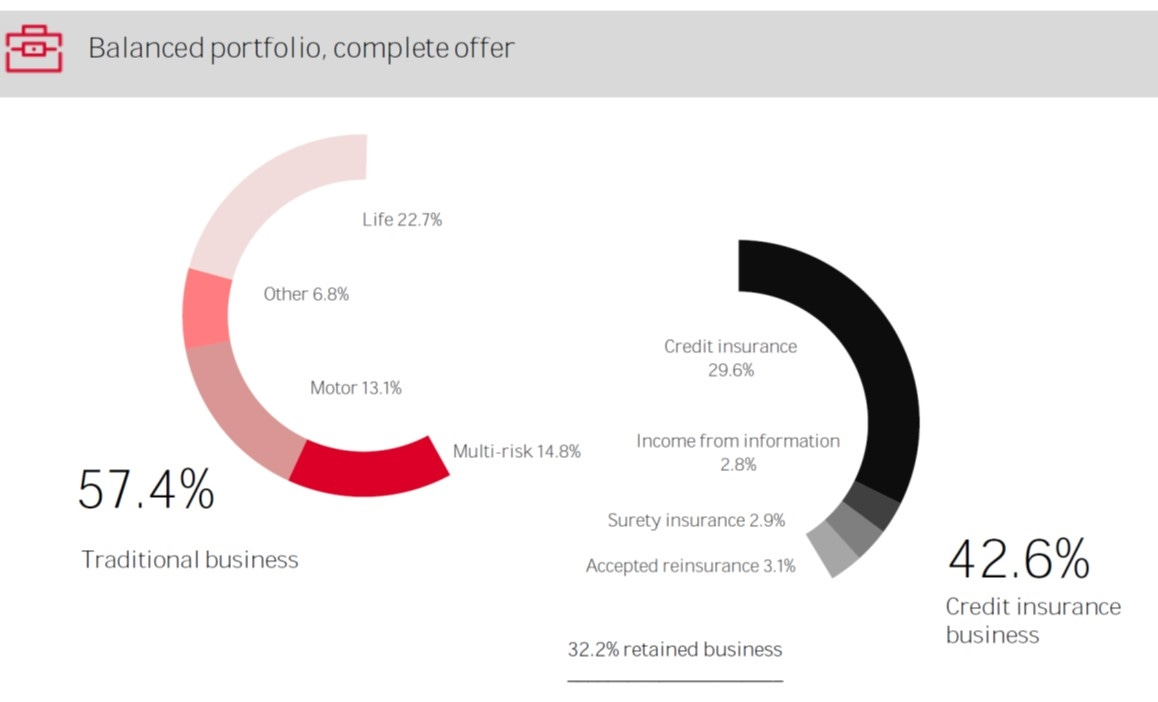

Grupo Catalana Occidente (GCO:SM) is a 150-years old Spanish insurance company operating across two lines of business: traditional insurance (P&C and life) and credit insurance (the coverage of commercial credit risks).

GCO is the fifth largest insurers in Spain (~5% market share), but by far the #1 domestically in credit insuran…