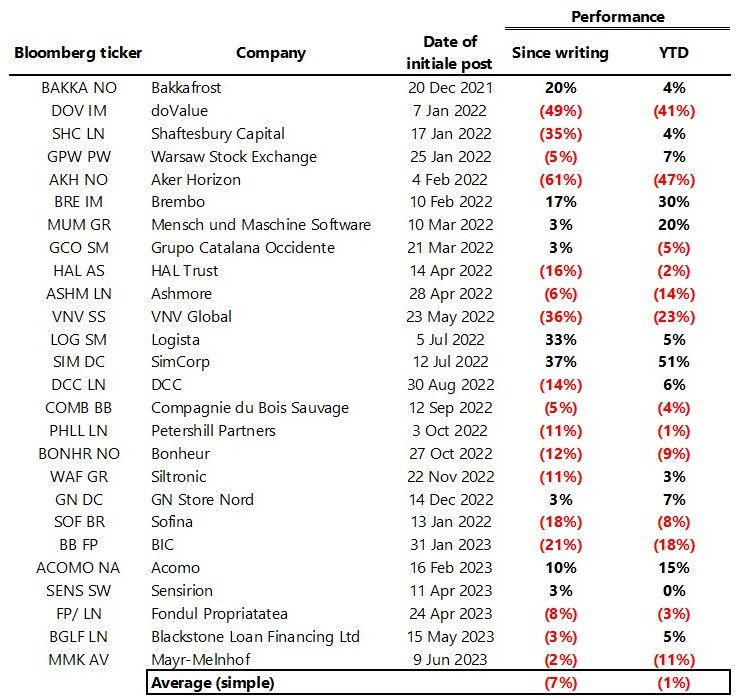

Performance recap

For all stocks presented

A quick recap on the performance of all companies discussed in this Substack since its inception, and also some comments –not for all of them - on what has happened since the original post.1

The simple average is negative -7%, so if you are looking mostly for long ideas you might want to con…