Headquartered in Turin (Italy), Reply ($REY.MI) is an information technology consultancy that provides system integration, application management and digital transformation services.

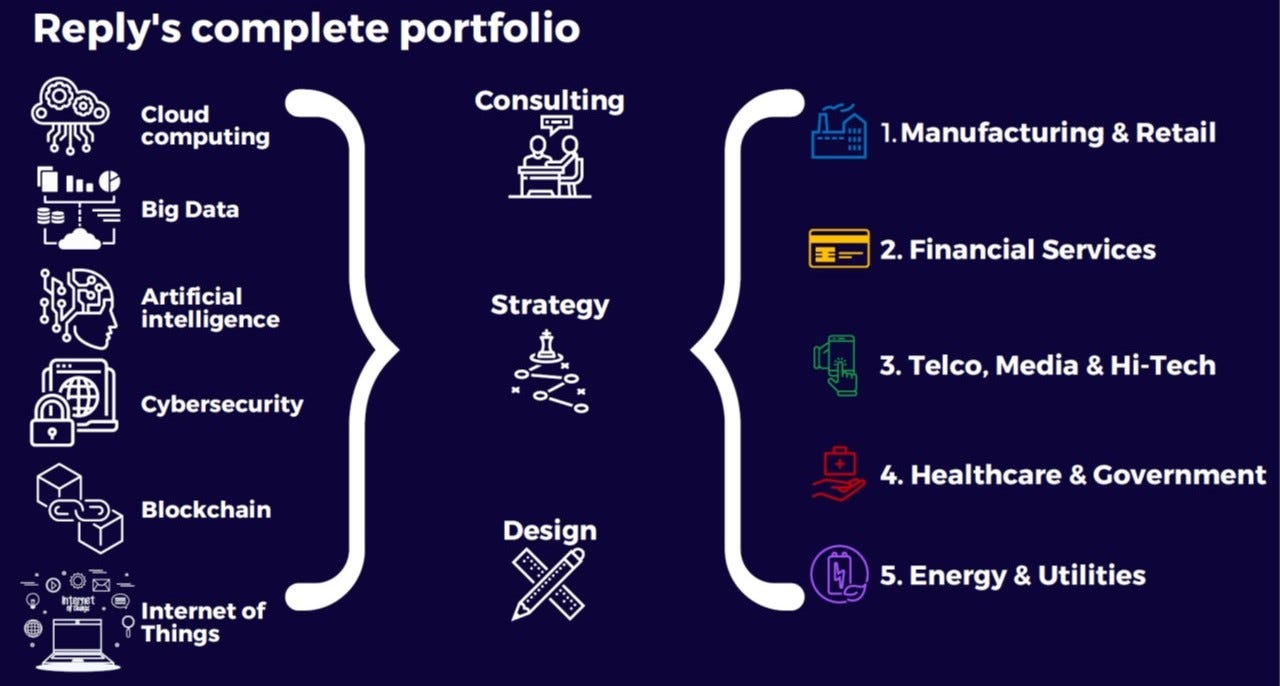

Its core business is combining design and processes and offering high-end solutions based on cutting-edge technologies (IoT, Cloud Computing, Big Data, AI, Cybersecurity).

Reply was founded in 1996 by a group of managers - led by Mario Rizzante - who left the security of a large organisation (Atos) to implement a new concept around numerous small teams that function as independent companies under a single corporate umbrella.

Reply listed shortly after and then expanded in Germany (2005), the UK (2008) and more recently the US (2018) and China: this was achieved mostly by strategic M&A transactions to complement its existing offering and expertise.

The Rizzantes still retain control of the business: Mario (75 years old) is Chairman, while his daughter Tatiana (53) and son Filippo (51) are, respectively, CEO (since 2006) and Chief Technology Officer (since 2011). They both have an extensive background in computer science and technology. Alika, the family holding company, current holds ~40% of the shares (but 57% of voting rights), with the rest being free float.

Consultancy: a varied and often nebulous market

The consultancy universe is both vast and disparate: classifying companies is not an easy task, as barriers have become blurrier with time and due to the appearance of numerous new players. Definitions are flexible, sometimes overlap, and definitely overlook some subtleties.

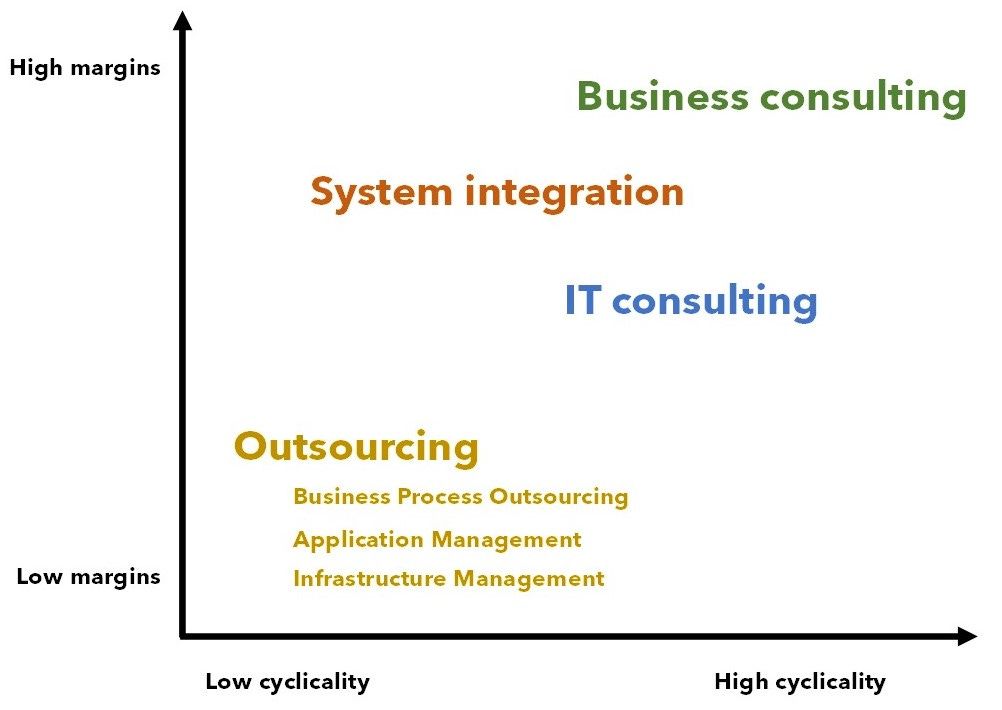

On a high-level, IT services can be divided into three main areas that mirror the lifecycle of a project: 1) consulting = advising on what needs to be done; 2) system integration = the building and implementation of what needs to be done; and 3) outsourcing = the management of the solution on an ongoing basis.

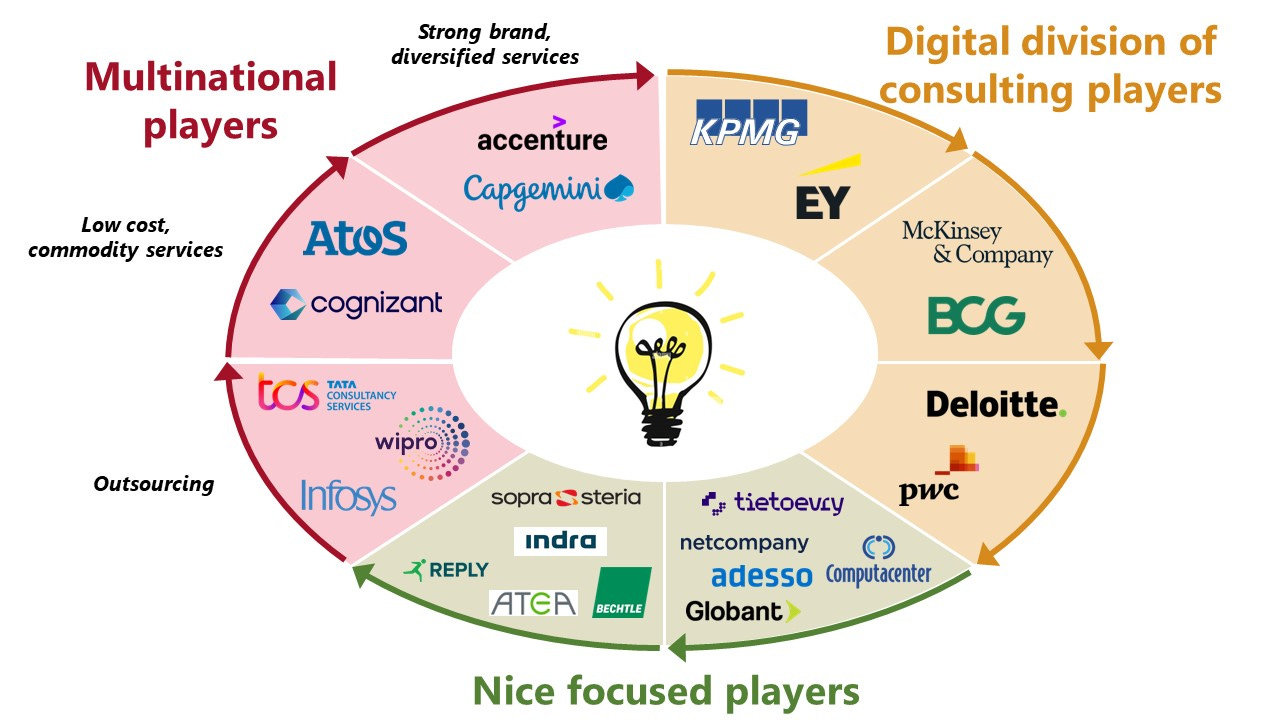

Another way is to classify companies based on their origin: many were not originally a core business for their parent, but were actually generators of additional business; therefore, this sort of categorisation provides an idea of the orientation/specialty of a consultancy firm.

Strategy: these are the most prestigious players, dedicated almost exclusively to high-end missions. The top three players are also the most famous: BCG, McKinsey and Bain & Co. However, there are other well-known players, such as Roland Berger, AT Kearney or Oliver Wyman, each with its own specialisation

Independent generalist players, which offer a wide variety of solutions and are able to address most of their customers’ needs. This includes BearingPoint, PA Consulting, Eurogroup Consulting and many more

Consultancy subsidiaries of IT players (such as Capgemini and Atos), which are sometimes the result of the acquisition of external consultancy firms

Operators that mix IT and advisory services, such as Accenture and IBM Global Business Services

Consultancy subsidiaries from the auditing Big Four (EY, Deloitte, PwC, KPMG), that provide services outside their traditional financial advisory purview

Smaller players who specialise in a very precise field, such as Reply, Atea, Netcompany, tietoEVRY, …

The various IT services areas offer different potential margins and also show different economic cyclicality. Advice given to customers on the strategic direction have the highest margins, but few new IT projects see the light in bad times and the demand for consulting falls away. Systems integration also come with relatively higher margins thanks to the critical and time sensitive nature of the service, and it falls in the middle ground when it comes to cyclicality. Because of the long contracts, the outsourcing business is the least cyclical (and since outsourcing is done to save costs the service could even be countercyclical with growing demand in harsh times), but margins can be fairly low.

A structuring trend: the digital transformation

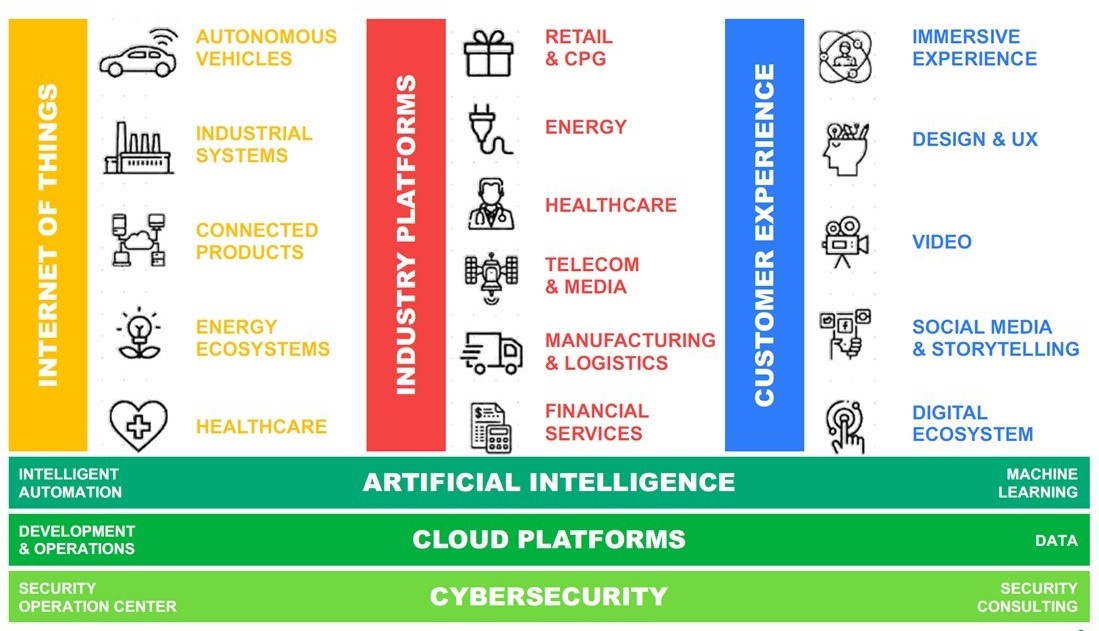

One of the most structural trends is the so-called digital transformation, an already worn-out catchphrase that is nonetheless a reality for many businesses. To put it simply, it refers to adapting “old school”, rigid business models and IT systems to the new technological landscape, which is characterised by openness and immediacy, as is perhaps best illustrated by the smartphone. For companies, this means first connecting internal IT systems - which are sometimes decades old and have been gradually modified with successive patches - to the outside world and especially to the mobile-based ecosystem.

Needless to say, despite the old system not having been designed modularly or even on an open architecture, a client’s business cannot be shut down during the transition to a new system. In addition, these transitions require a company’s employees to use modern, digital tools (not only a computer and an email account) and to fully digitalise (internal processes, collaboration modes, working environment, etc.), in order to be responsive to customers’ needs. The digital transition is not only a transition of technology, but more importantly a cultural transformation too.

For consultancy companies, this brings numerous business opportunities: in addition to helping the company establish a new digital roadmap, select and implement new systems (which implies a wide range of domains, from infrastructure design to data security), consultants will also be required to manage the human side of the transition, i.e. drive the acceptance and assimilation of the new tools by employees and design a transition programme for the workforce to be replaced by automation or by AI.

Reply: a peculiar business model

Reply’s key strength is its unique decentralised network of around 160 highly complementary subsidiaries (their own definition is as “a shopping mall of specialised boutiques”), each with its own specialisation, brand and competence, and – more important – a significant autonomy when it comes to hiring, spending decisions and P&L accounting.1

This network derives from the expansion due to the continuous M&A activity, as well as the various partnerships undertaken over the years, that have allowed it to consolidate its business, becoming one of the top IT services companies in Europe.

This decentralised model allows for the benefits of a large enterprise (sharing of knowledge and "on field" experiences) without being static or monolithic but rather maintaining a start-up entrepreneurship: each subsidiary can leverage the corporate brand and rely on financial support,2 while also maintaining close geographical proximity with customers, providing tailored services in their respective competence areas and a flexible structure to promptly react to the dynamism that characterises the digital market.

Competencies are grouped into “clusters” based on geographical, technological and industrial criteria (there are currently 20 clusters), each managed by an operating partner who reports directly to top management. They are also appraised on the economic performance of their reference businesses: 50%-60% of their compensation is variable, mostly based on achieving margin targets rather than revenue growth. Reply wants managing partners to focus on profitable businesses, not intellectual satisfaction.

Despite being smaller than the biggest players in the industry, this organisational model has allowed Reply to remain competitive thanks to the innovative solutions that it periodically adds and provides to its customers, thus creating a high loyalty to the brand. Reply acknowledges that its network structure might not be built for economies of scale: but they are also very clear that they are not interested in doing big outsourcing work, so they do not compete directly on scale/pricing with the Indians (Wipro, Infosys, ….). They are also not interested in building their own cloud offering.

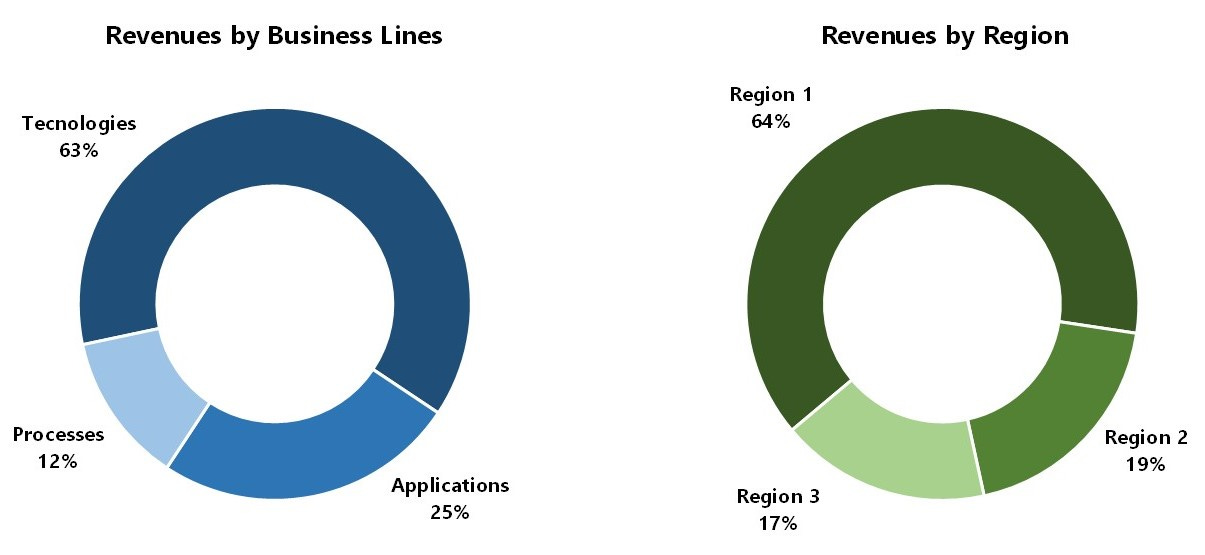

Reply’s offer covers three areas of competence:

Processes: understanding the use of technology to introduce new enabling factors; define, optimise, monitor and integrate business processes in fields such as Human Resource Management, Accounting/Finance and Supply Chain Management

Applications: designing and developing application solutions aimed at meeting core business needs

Technologies: optimising the use of innovative technologies and solutions to guarantee maximum operational efficiency and flexibility for clients

Region 1: Italy, US, Brazil, Poland, Romania, China (Nanjing), New Zealand

Region 2: Germany, Switzerland, China (Bejing), Croatia

Region 3: UK, Luxembourg, Belgium, Netherlands, France, Belarus, Singapore, Hong Kong, Malaysia3

This very peculiar regional segmentation is due to the types of contracts that Reply offers:

“Turnkey projects” (around two thirds by number of contracts): Reply delivers the service at a fixed agreed-upon price defined at the inception of the project; revenues are recognised over time based on the progress of the services provided

“Time & material” (the remaining third): the price depends on the customers’ requests on a time-spent and number of consultants basis

Turnkey projects represent the majority of contracts in Region 1 (Italy, US), while Region 3 (UK, France, Netherlands) primarily makes use of contracts based on the time spent; Region 2 (Germany, Switzerland) is almost equally divided between the two types.

Customers are mostly large/medium corporation in a few well-defined sectors. Although in any given year there are typically several large contracts, these are often made up of a number of services supplied by different group subsidiaries.

Telco & Media (21% of 2022 revenues): characterised by continuous transformation, the operators involved have made massive investments in conventional assets, but without redefining the underlying technologies. Reply supports telcos in their transformation to software-based operators, starting with the redefinition of their technological foundations and creating cloud platforms capable of managing the entire technological stack, from network access to front-end channels, and in the definition of new business models enabled by composable architectures.

In the media sector, publishers are reacting to the profound crisis of traditional channels, which is leading to a search for innovative digital solutions and new products that can satisfy customer preferences. Reply is supporting relevant European players in the process of converging offers, contributing to the design and implementation of new bundles made up of fixed/mobile broadband connectivity, value-added services and premium editorial or TV content.

Case study - Deutsche Telekom: software-defined networks

DT’s program Access 4.0 aims to deploy geographically distributed mini data centres at the network edge to produce broadband Internet and VPN access for its customers. The program endeavoured to refine the way networks are built and deployed: traditional hardwired systems are replaced by open, disaggregated and microservices based technologies. Starting with a prototype in 2018, Reply co-developed, conceived and implemented the global productization strategy for the new A4 platform, rolled out in 2020.

Financial Services (30%): in addition to regulatory developments, technology has been the main driver of change in the sector in recent years, with financial institutions increasingly becoming ”tech companies”: to be successful they must innovate their entire value chain (sales/distribution, operations, procurement). Reply’s works range from digital branding to the implementation of apps, and from the development of a new generation of multi-channel portals and touchpoints to the complete redefinition of the underlying technological architectures (online payments, IT security, retail credit and risk control, …).

Case study - Nexi: cloud and machine learning

Reply enabled Data Analysis and Machine Learning on AWS Cloud for the provider of digital payments, bringing quantity and quality of data and leveraging artificial intelligence-based technologies, resulting in major impacts in Nexi’s capabilities in areas like fraud, risk management, marketing and operations, in a safe and compliant way.

Case study - BPER Banca: Valentina virtual assistant

BPER offers traditional banking services with ~1,200 branches across Italy. In 2019 it decided to introduce artificial intelligence approaches into their business to facilitate day-by-day activities and to automate operations still done by human employees. Reply built Valentina, a natural language holographic avatar with the goal to help customers by providing a near human support for different operations. Upon entering the digital branch, the customer identifies himself with a personal smart ring and is greeted by Valentina's 3D avatar that accompanies him in the self-service area and guides him through the operations like information or dispositions (withdrawal at the counter, request for a bank transfer).

Manufacturing & Retail (33%): Reply is mainly active in the management of supply and purchase activities, the design and implementation of control and planning systems based on the new generation of cloud ERP, the planning and control of production units and the design and definition of logistics supply networks. It has defined a specific service offering for the retail sector that combines ecommerce and multi-channel consulting with the design and development of solutions that integrate web, mobile, call centre and in-store services and in which digital devices, innovation and physical places are brought together to create an engaging and consistent customer experience.

Case study - Lavazza: guarantee process quality

The production process of Lavazza (one the world’s leading coffee roasters operating in more than 90 countries through subsidiaries and distributors) is based on high value raw material and the quality of the final product to stay ahead of the competitors. Tracking the product quality levels and monitoring the machine working state in real-time allows the production managers to identify potential anomalies, preventing low production quality. Many variables (time, temperature, …) impact the quality of the output; in addition, the production line needs to manage different types of products in order to guarantee efficiency and timely launch of new products. Lavazza worked with Reply to design a product which could fit their needs to predict the results of the tests performed on the production line to guide their operator’s activities: the data are collected from heterogeneous sources in a single AWS Data Lake and processed using Python.

Case study - IKEA: an outcome-based roadmap

Ikea was moving from a traditional five-year planning model to an iterative approach to change that would hold investment/planning cycles every four months, enabling them to delivery consumer products and services alongside technology modernisation, and remaining relevant, agile and profitable. The core of IKEA’s Digital Transformation was a switch to a capability based organisational structure for the IT function. Reply worked with stakeholders from Roadmap Leaders to Product Managers and Senior Leadership across the organisation to articulate requirements, key challenges and ambitions. It introduced Objectives and Key Results (OKRs), a simple goal setting framework that creates alignment, supports autonomy, and allows measuring impact. Ikea gained a new investment planning framework prioritising small and frequent work packages that are capability-based, and outcome-focused. This approach allows quick course correction to adapt to changing market factors.

Energy & Utilities (8%): the sector is currently undergoing a profound transformation with regard to the models used for generating, distributing and selling energy. Reply supports companies in defining new operating models and implementing projects in line with the main technological trends (blockchain), through sustainable solutions that comply with the regulations of the sector. Aspects covered include smart metering, smart grid management, real-time pricing and demand response.

Case study - Enel: Quantum optimisation

With a presence in 30 countries and a network supplying 74 million clients worldwide, Enel has an impressive technological infrastructure to maintain and complex internal processes that require continuous optimisation and that make the efficiency of operational resources the key to business development. Reply has created a QUBO (Quadratic Unconstrained Binary Optimization) model that identifies an optimal plan for assigning maintenance work to teams. In a few minutes, the model can identify a schedule that maximises the amount of time spent working, while also minimising the time spent on the road. The quantum algorithm allows to quickly plan the maintenance work performed by units operating throughout the network, making the use of resources more efficient and thus reducing costs.

Government & Healthcare (7%): there has been an increasingly strong focus over recent years in the health and public administration sectors on cutting costs while still maintaining quality. Reply’s activity is strongly oriented towards the design and implementation of an interoperable public administration, with the integration of big data and open data, artificial intelligence and deep learning, cloud and new architectures. The technologies are applied to improve the relationship with users and govern internal business processes.

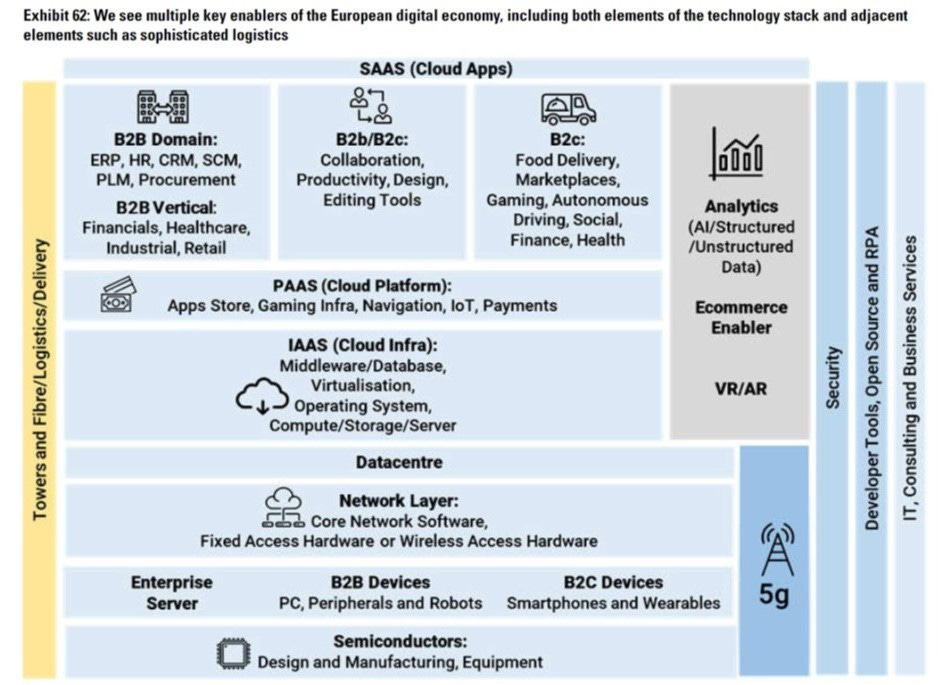

Platforms, Products and R&D

Not being a pure software distributor (rather: it supports customers for the entire implementation phase of each project), to offer the most suitable solutions Reply has established important partnerships with the main global vendors.4

A second selling point is the continuous process of research and promotional initiatives to support customers in the efforts to adopt new technologies. These platforms represent application solutions to respond to new needs generated by the trends in business and innovations.

Axulus Reply: a solution for cloud-based industrial IoT operations management, which provides different predefined frameworks on specific use cases for the digitisation of manufacturing companies

Brick Reply: a platform dedicated to the digital transformation of industrial operations

China Beats: a marketing intelligence and social listening platform dedicated to understanding the Chinese market and its vast data ecosystem, connected to all major Chinese e-commerce platforms, search engines and social media.

Discovery Reply: an enterprise digital experience management platform, which centralises the management of images, video, audio, documents and data

Lea Reply: a platform designed for making supply chains efficient, agile and connected

Pulse Reply: a data-driven insight solution that combines data science and marketing intelligence activities in an agile dashboard, including advanced data modelling and visualisation capabilities, it’s designed to allow users to monitor business performance and support forecasting

Sonar Reply: a solution for data-driven trend research, developed in collaboration with the German Research Centre for Artificial Intelligence: this solution was designed to offer a user experience similar to that of search engines and is intended not only for data analysis professionals but also for researchers and journalists

TamTamy Reply: conceived as an Enterprise Social Network platform to facilitate communication and collaboration within companies, TamTamy now supports several projects dedicated to training and human resource management

Ticuro Reply: a platform solution for the connection of digital healthcare, it enables processes to support prevention and continuity of care even remotely

X-RAIS Reply: an artificial intelligence solution to support radiological diagnosis processes through deep learning

It also has its own labs, where prototypes and innovative ideas are developed and clients can book their own workshops:

Area 42 (Turin, Italy): to explore the potential of the most innovative robotics, advanced mobility, virtual reality and metaverse technologies

Area360 (Milan, Italy): dedicated to the development and testing of real-time 3D interactive immersive experiences and virtual and augmented reality solutions

Cybersecurity Lab (Cologne, Germany): to evaluate different security scenarios applied to contexts such as adaptive cloud security, secure software development lifecycle, network security infrastructure, application and data security and security assessment.

Immersive Experience Labs (Munich, Germany): to test various areas of application of extended reality, from sales to marketing, from design to production, from maintenance to operations, and up to professional training.

IoT Validation Lab (Turin, Italy): used to design, integrate, validate and implement IoT connectivity solutions and related products

Test Automation Center (Turin, Italy): using proprietary AI/ML-based validation techniques, it monitors the quality of business-critical products and services throughout their entire life cycle

Growth strategy: organic + deliberate M&A

Reply’s strategy remains the same as at its foundation: grow a diversified customer base to exploit technology to its maximum capability while maintaining a high customer retention.

End-to-end services: design, implementation and operations

Vertical markets core processes knowledge

The group’s main focus is on developing and growing expertise in all the most innovative areas of IT: they want to be an innovative niche player in high growth markets. That way they can charge “premium prices for high-end services” and avoid commodity areas which are more price competitive.

Reply thinks they can grow organically 10% p.a.: not necessarily by taking market shares from competitors, but just growing with the underlying market. Growth is coming not only from acquiring new clients but, to a larger extent, in step with its existing customers’ growth.5 Customers call on Reply to ask for solutions to newer problems, and this has proved to be the best driver of the company’s growth.6

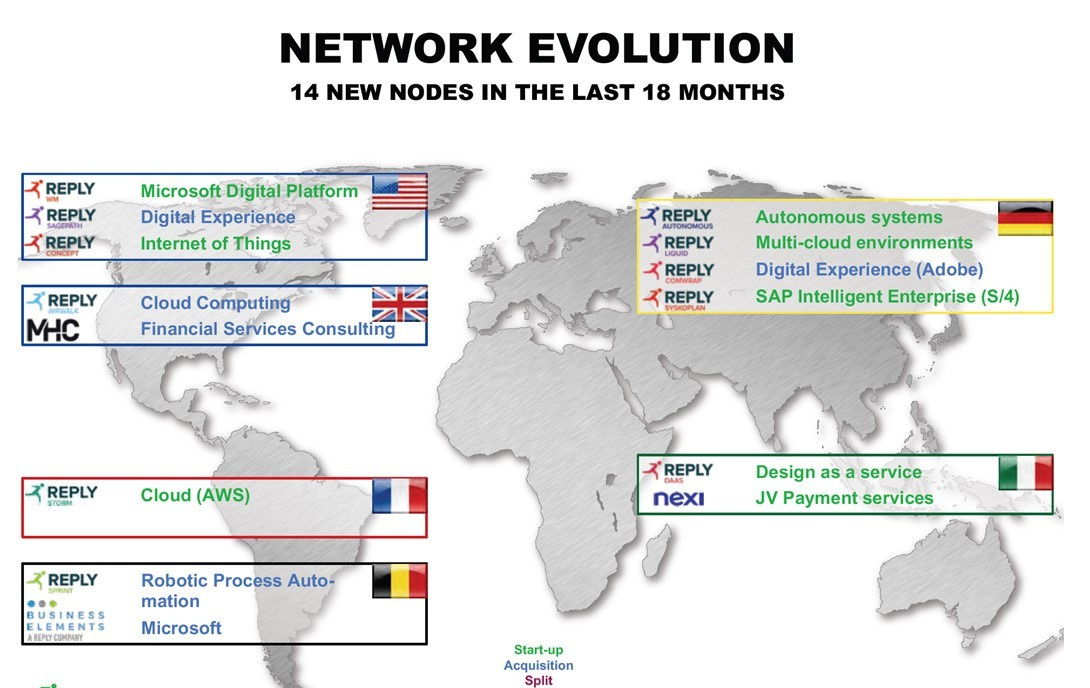

Being constantly looking for innovation and specialisation, the company adopts an M&A policy that consists in building solid knowledge bases in each sector it deals with by recruiting companies it considers strategic: Reply focuses on bolt-on acquisitions rather than transformational deals which would not fit the network model. As such, Reply’s network has grown over the years through both the seeding of new start-ups and the full take-over of niche market leaders (“build-and-expand”). This acquisition strategy results in a "light" integration process of the companies within the group network.

With a medium term goal for Italy to account for less than 50% of total revenues, management has a clear vision of the new regions that are considered strategic (UK, Germany, France, and some areas of US, while the company is also starting to look at Belgium), which are also the countries that saw the biggest focus in terms of M&A over the last 10 years.7 As the management stated: “To win the projects with large multinational corporations it is necessary to be physically in the reference markets. Furthermore, innovation comes from interaction with the different end markets and the customers”.

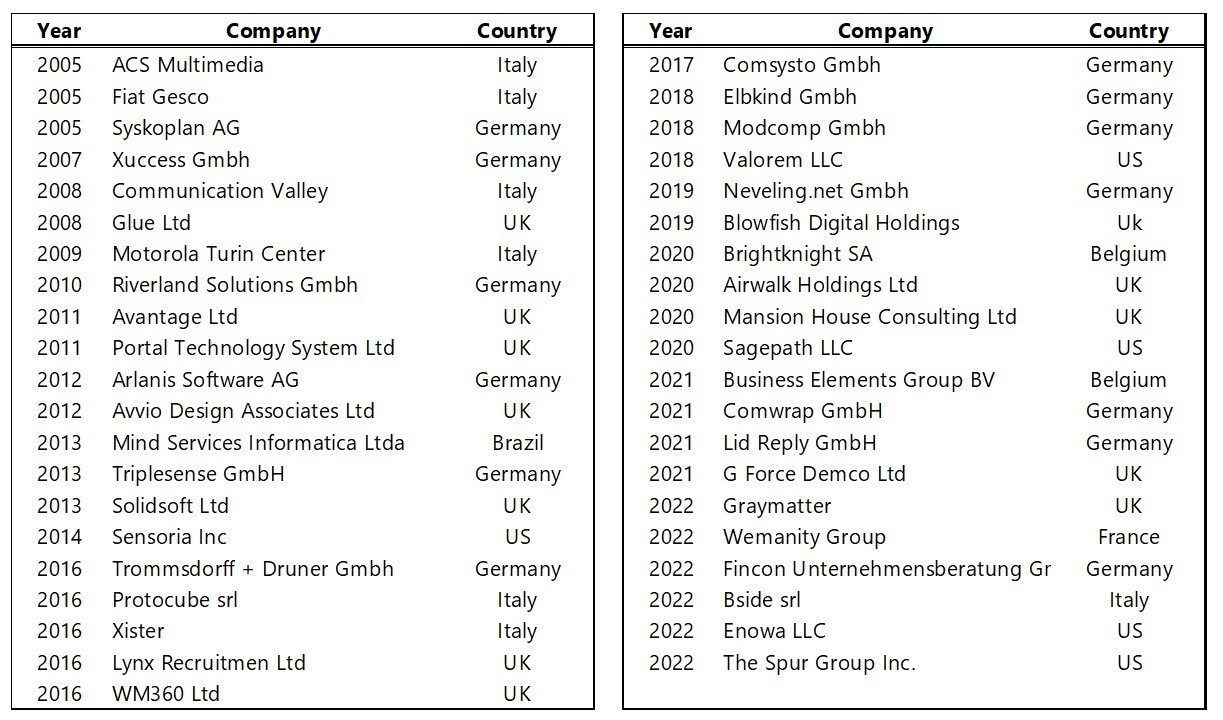

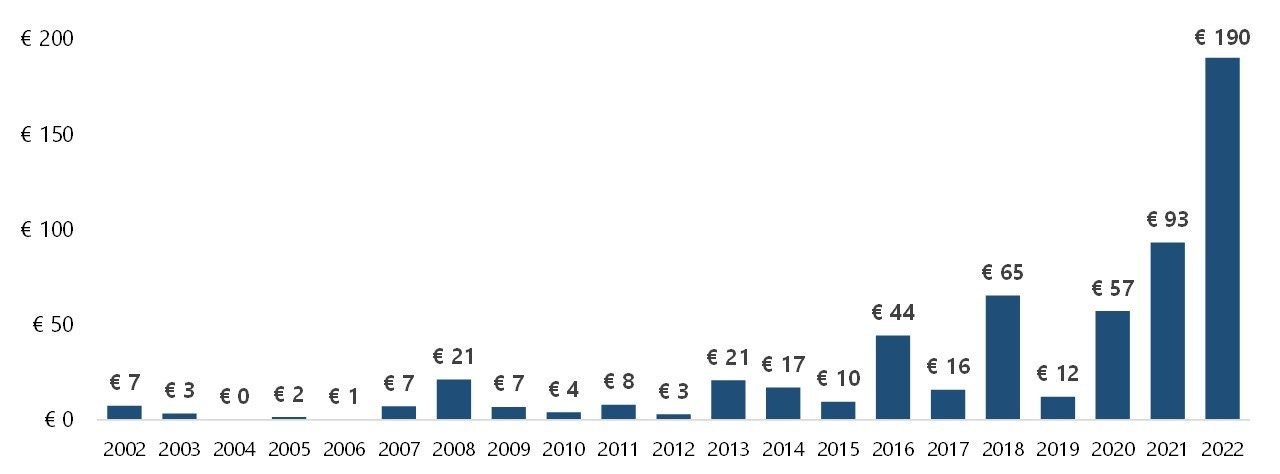

Since 2002, Reply has spent almost €600 million on acquisitions, with a marked acceleration since 2018. The biggest deal was consummated last year, when Reply acquired 100% of Fincon Unternehmensberatung GmbH, a German consulting company leader in digital transformation projects for the banking and the insurance industry, for an initial consideration amounting to ~€120 million. All other recent acquisitions have generally been in the €5 to €30 million range.

Prices are not always disclosed (and targets’ metrics almost never), so it’s difficult to ascertain what kind of multiples they paid for the international expansion: according to Intermonte, in discussion with management they stated that Reply has never paid a double-digit EV/EBIT multiple and has no intention of targeting competitive or overpriced deals.8

In October 2014 it also launched Breed Reply, a new incubator for funding, accelerating and supporting the growth and establishment of ideas and start-ups around IoT across Europe and the US. Based in London and with offices in Italy and Germany, it offers three fundamental services: funding at "seed" and "early stage" level; considerable support with significant know-how transfer of business, managerial and technological expertise; and thanks to Reply’s ecosystem, medium-term involvement to establish the start-ups in their market.

Radiography of the market: regular (and secular) growth

The consultancy market has been developing nicely since the 2008 crisis, and its size can vary depending on what is included within the perimeter (especially in IT-related domains): it tends to enjoy mid-high single-digit growth rates thanks to economic growth.

The European IT service market is facing a secular trend of growth, further accelerated by the Covid pandemic which made digitalisation every company’s priority. The consultancy market for financial services is also thriving, under the combined influence of shifting regulations and the digital transformation, which has turned the old business models upside-down amid the rise of the fintech players. And public services are actually not that mummified! At first glance, public services would seem to be a less obvious choice, given the recent wave of cost-cutting programmes, as well as the legendary late payment periods. However, this segment is more vibrant that it initially appears, driven by modernisation of the state policies.

Estimates for the size of the markets varies depending on who you ask and what they include in their definitions. The entire European IT market is probably around €450 billion (US is bigger, while Asia is still very marginal for Reply), although Reply’s TAM is much more limited to: 1) IT consulting (€10 bn), and 2) development and system integration (€50 bn).

The market is expected to face a considerable boost from the increasing adoption of digital enablers. This new digital wave will trigger a rise in demand for system integration services, as an increasing number of companies will need to implement these new technologies to stay on top of innovation. Indeed, historically, the revenue growth of companies like Reply has always been strongly correlated to the growth of the digital technology market, rather than to the size of the market itself.

And despite the push towards digitisation all over the world, the Digital Economy and Society Index (DESI) shows that some large European countries are still below the region’s average (Italy, in particular in the integration of digital technology), while others (Germany and France) also lag the Nordics.

As part of the Multiannual Financial Framework (MFF) for 2021-2027, significant European funds are marked for digital initiatives, with AI, cybersecurity, and supercomputing among the core areas of focus. The European Commission has set up the Digital Europe programme to accelerate recovery and drive the digital transformation of Europe over the next few years by unlocking an overall budget of €7.5 billion. In addition, Horizon Europe, the European funding programme for research and innovation, will continue the work of Horizon 2020 but will be strengthened to fund research in health, resilience, digital and green transition. It includes a dedicated budget for Digital and Industry to develop research and high-end innovation in enabling technologies, with a total budget of €95 billion.

The MFF, together with the €750 billion in extraordinary recovery instruments contained in the Next Generation EU plan (with about 15% to be allocated for IT services/products spending), will help transform the region by supporting the European Green Deal and digital transformation. Italy is set to be one of the largest beneficiaries of the recovery instruments and should receive €223 billion from NRRP (“National Recovery and Resilience Plan”): over €46 billion are destined to “digitalisation, innovation and competitiveness”, and another €32 billion to infrastructure for sustainable mobility.

At the end of the day, it’s a people business…

In the IT sector, human capital is the key asset: fundamentally, this means being able to attract and retain the best people.

Reply employs more than 14,300 people in 16 different countries (one of the largest in Europe) with partnerships with 152 universities.

The IT industry is highly dynamic, offering many opportunities to create new market niches and requiring quite low entry investments. However, reputation is a critical aspect, as customers give high value to strong brand identity and a solid track record.9 Achieving brand recognition is paramount, so entering the market on the “high end” is not easy: new entrants must invest significant time in building a strong reputation and recruiting skilled personnel.

Reply has today a much stronger brand than 10 years ago: it enjoys an established international presence and can benefit from a number of partnerships with the most important universities in Italy and Europe. It has developed an internal performance-based compensation scheme: compensation for managers is heavily results-based, and it grants the most successful people with a rapid career path and a rewarding professional environment. As previously stated, the majority of their compensation is variable: of this, 70% is to achieve margin targets and only 10% is based on revenue growth. While Reply has traditionally identified EBITDA as the prevailing performance indicator for both the short- and long-term remuneration, in 2020 the policy was revised to include additional performance indicators for the variable medium/long-term component of remuneration (total return to shareholder, FCF from operations, return on capital employed). It has also introduced a period of deferment of the payment of the variable components and provisions on the application of “claw back” mechanisms.

Recruitment is focused primarily on young graduates: the relationship between Reply and universities is developed through regular partnerships, such as industrial placements, dissertations, and participation in lectures and seminars. Through social networks and challenges (“Student Tech Class” or “Life at Reply”), the company uses the experiences of customers, students and employees to make products more adaptable.

Financials

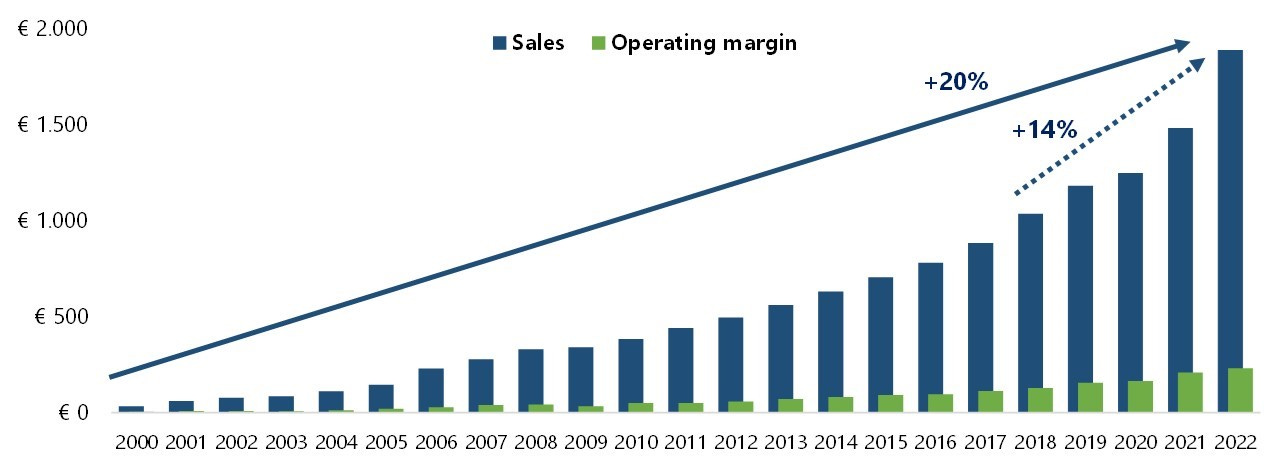

Sales have grown from €30m at the time of the IPO to around €2 billion today (+20% p.a., slightly less +14% p.a. over the last 5 years): according to the company, ~80% has been organic, with the rest coming from acquisitions, and Reply has been able to grow topline even in 2009 and 2020. Operating profits have followed accordingly (+15% p.a. over the last 5 years) to reach €230 million in 2022.

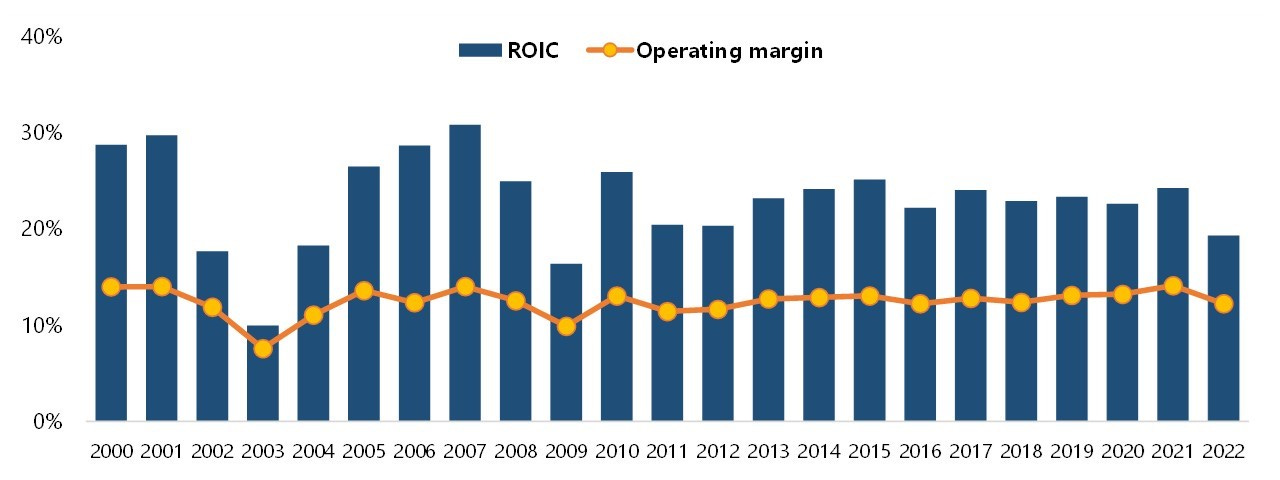

ROIC and operating margins have been steadily in double digit, despite the significant increase in operations (support staff, admin, …): this is a typical (tangible) asset-light business with limited operating leverage. Personnel expenses are the main driver of margins: including commercial and technical consulting (sub-contracting agreements and external consultants), these costs represent almost 90% of all operating costs and 75% of revenues.

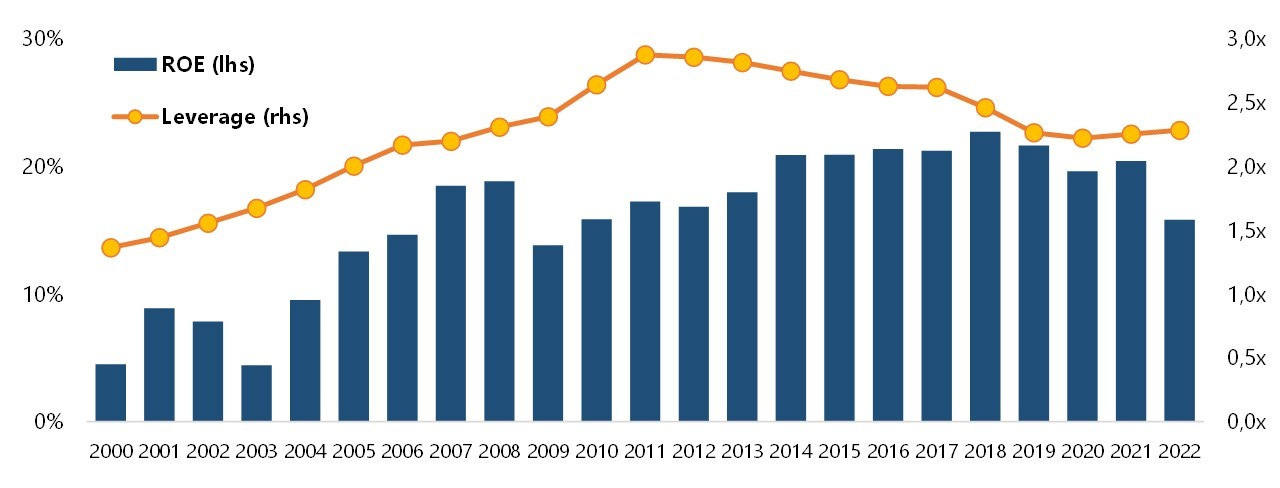

ROE is also high without the need for much leverage. Net debt is currently around €70 million, and this is including a €130 million estimate for future earn-outs / buyout of minorities (otherwise the company would be net cash positive): these future “payments” are well covered by cash flows from operations, around €180 million at the current run rate.

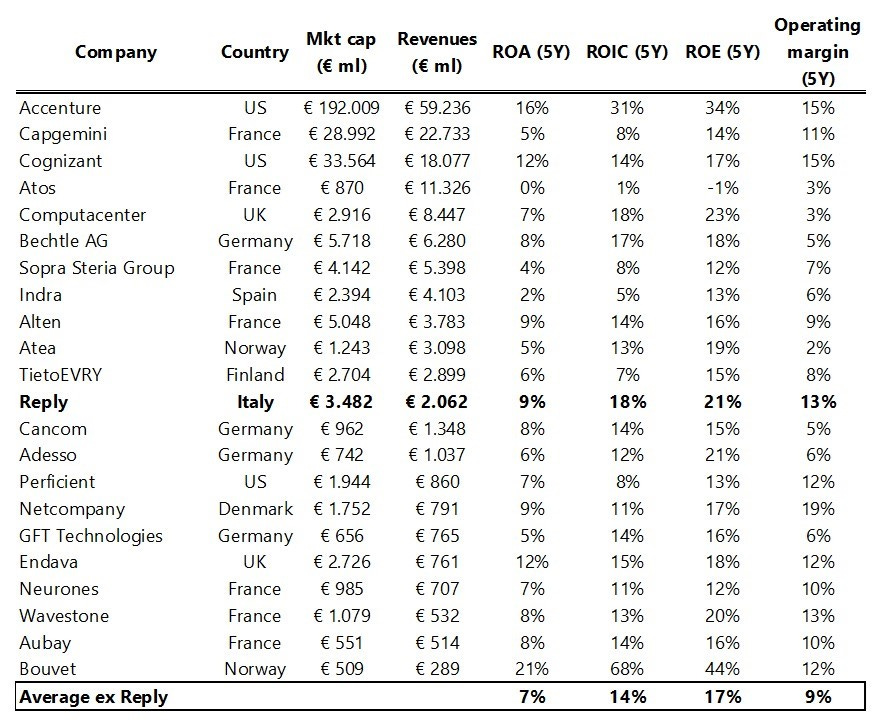

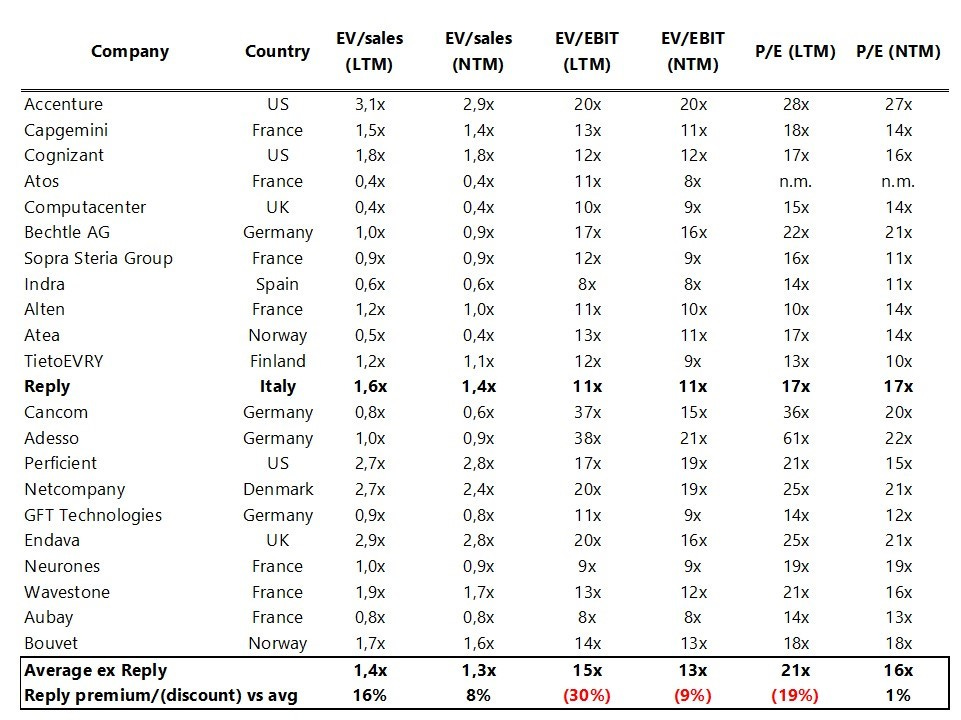

As previously said, the consulting world (even for just IT) is vast: there are dozens of competitors, from small to large to giants like Accenture, both in Europe and even more in US. Not all of them compete with Reply to provide the same services: below is just a sample of companies that are similar for both service offering and geographical reach.10

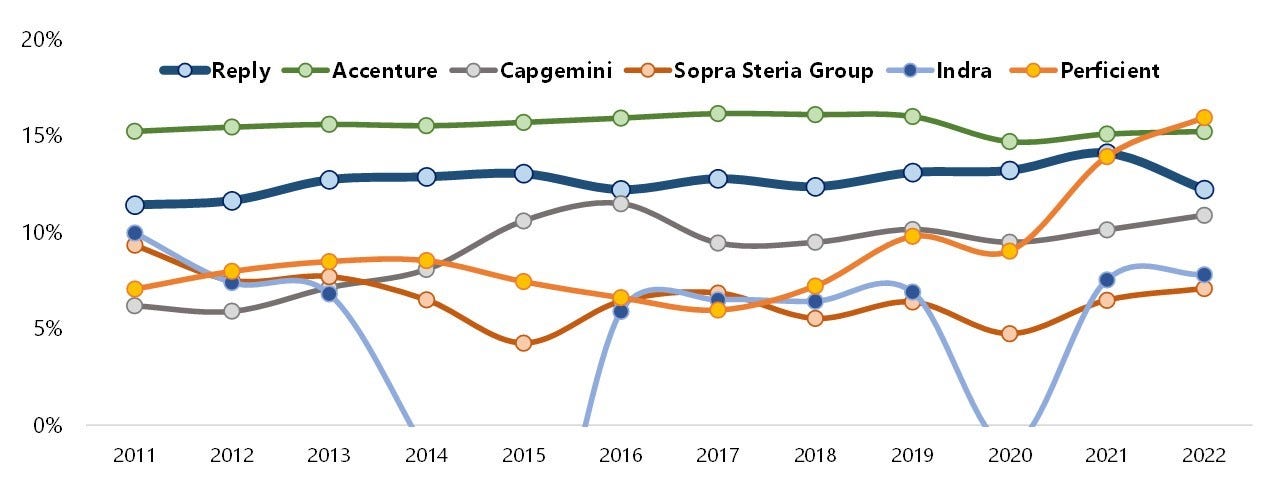

Reply is in the top percentile for both return on capital and margins. Overall, this is quite a commoditised sector, where it’s difficult to really differentiate your offering: margins tend to drift down towards single digit, if you are good you are at low double digit. Reply’s margins are not far away from those of Accenture and are both higher and more stable than at European peers like Capgemini, Sopra Steria and Indra.

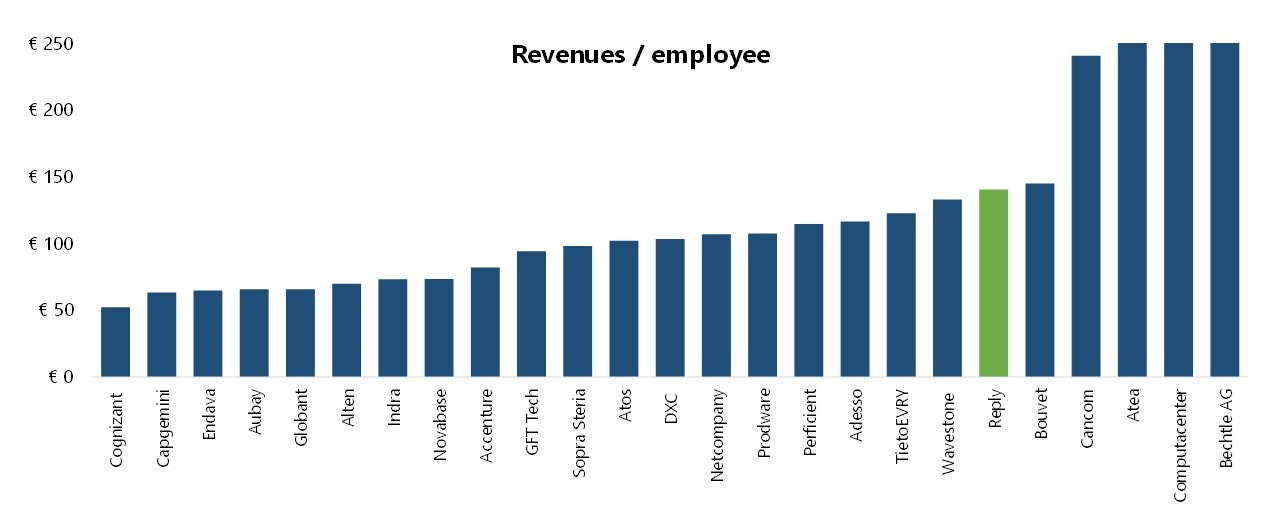

Reply is also among the most efficient, with high revenues per employee (same for EBIT/employee, not shown in the chart): small companies are more “productive” as they have a larger percentage of front office professionals and less admin staff, while larger companies need more support personnel. Reply is kind in the middle, and it’s the most efficient of its cohort.

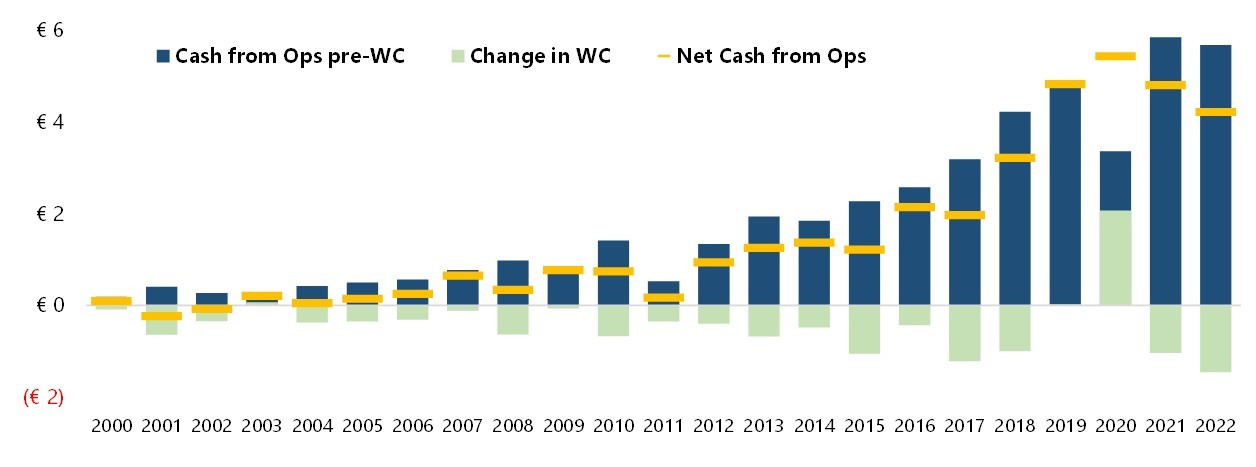

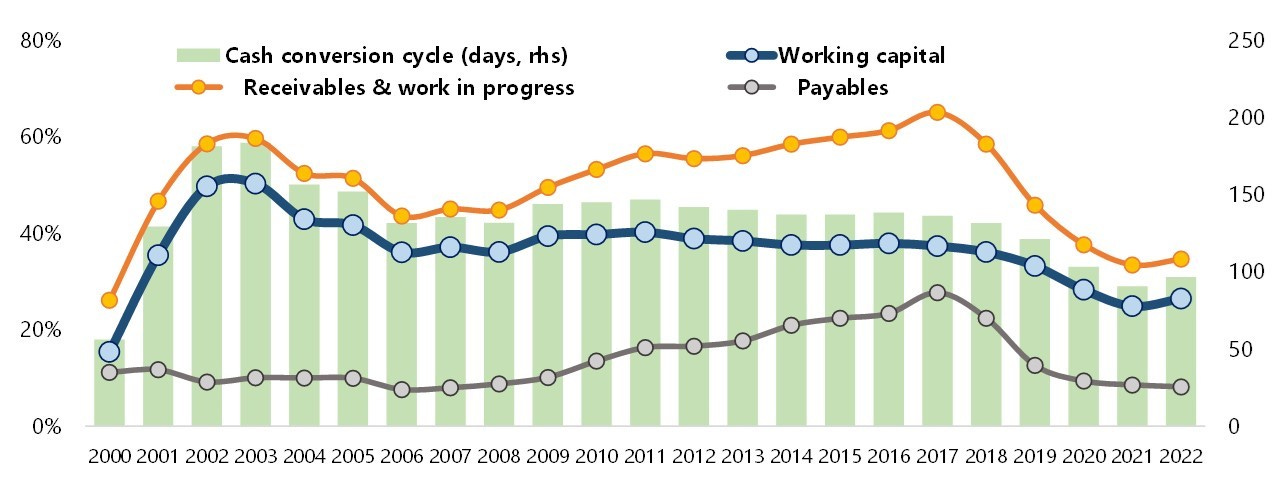

Cash from operations has been steadily growing and was positive even in 2009 and between 2011 and 2013 (a protracted period of recession following the Euro crisis), proving an extraordinary resilience to severe economic downturns. The swinging factor (i.e., what determines annual FCF generation) is however working capital.

This means that cash conversion will lag profits (with the exception of periods like 2020). This issue is quite common to the sector, with varying degrees depending on the types of projects undertaken: working capital as a percentage of sales is ~15% at Accenture, but 25%-30% at Reply and Netcompany. Reply is actively working to reduce it, with some success over the last few years.

More important, the sector is not as capital-light as it seems: it does not require a lot of tangible assets, but certainly a lot of (working) capital to grow. Reply’s own capital allocation over the last 10 years shows that cash generated from operations has almost entirely gone to support growth (capex, working capital, M&A: the latter is actually capex by another name, as they are buying R&D, customer relationships, ….). Shareholders got something but not much (as in “not much in hard cash but a lot in term of price appreciation”).

Reply’s policy is that “dividends follow profits”: around 20%-25% of net profit is paid as dividends, with the rest reinvested in the business (especially M&A outside of Italy). There have also been some sporadic buybacks (€7m in 2021 and €10 million in 2022), but they are marginal compared to dividends.

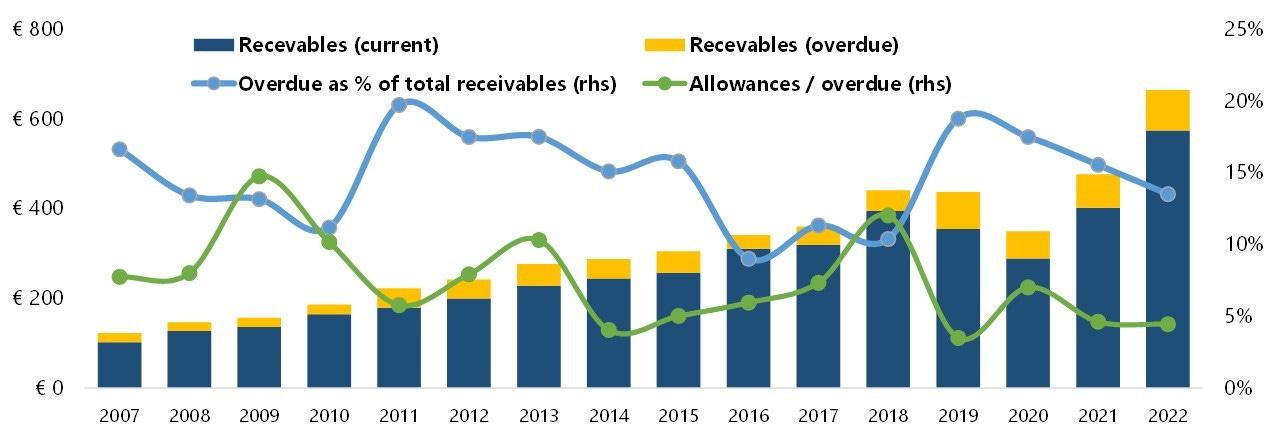

Are receivables a potential red flag? Not only they are a significant drag on cash flows, but those overdue represent on average 15% of total receivables (although the most part are overdue by less than 3 months): how come that Reply’s clients (mostly large multinationals) do not pay on time? And allowances for doubtful accounts are minimal (on average 7%) with respect to overdue receivables, and almost all concentrated in the “Over 360 days” bucket.

Companies do have some leeway in how to account for credits from customers, but is Reply too optimistic in its assessment? This would imply poor visibility especially in the cash flow statement.11

Valuation

Price has appreciated nicely since the IPO, but it has inverted since late 2021: it’s down 18% this year and more than 50% since the all-time high.

Part of the recent downturn is due to a (temporary?) slowdown in Germany (the recently acquired Fincon is performing below initial expectations) that has dragged organic growth down to 8% in Q2 (still up +15% YoY). EBITDA and operating margins have also come down, continuing a (negative) trend that was already noted in 2022.

Using the same universe as before, few considerations on the sector valuation (below):

There is a lot of variability in the multiples because of the different underlying business models and segments served (for example, pure consulting vs reselling of software/hardware)

US companies trade at a premium: not a surprise, a lot of European companies want to move to US exchanges because they think they deserve higher multiples

Reply is a bit expensive on EV/sales (justified by its better margins), but at a discount to the average on EV/EBIT and P/E.

Note (important): these numbers are from Koyfin, I personally use a different methodology to calculate EV by also including earn-outs in financial debt. Also, Reply’s income statement for 2022 includes €50 million (€36 million after taxes) for “net positive changes in the provision for risks and charges for contractual, commercial and litigation risks and to provisions allocated to adjust assets. In particular, an extraordinary provision allocated to operating costs and impacting EBITDA was reversed in full to take into account the economic repercussions linked to Covid-19” (basically, they included some costs in 2020 and reversed the provision in 2022). Koyfin’s metrics take operating and net profits as reported, but this item is non-recurring. With these two adjustments (EV and profits) my LTM multiples for Reply are EV/EBIT 15x and P/E 22x, and the discount to the average disappear (I can’t double check the multiples for all other companies, so take the conclusions from the table with a pinch of salt).

As further reference, in 2019 Capgemini acquired Altran Technologies for €3.6 billion, equivalent to EV/sales 1.6x, EV/EBIT 13x and P/E 17x (more or less where Reply is trading today), and few months ago Sopra Steria acquired Dutch company Ondina for €520 million, which equates to a EV/sales 1.2x, EV/EBIT 14x and P/E 21x. Finally, Cancom recently acquired KBC Beteiligungs GmbH for an EV of ~€200 million, which comes in at EV/sales of only 0.4x.12

Overall, despite the massive de-rating over the last couple of years, Reply is not exactly cheap (not even relative to the sector): current FCF yield is ~4%.

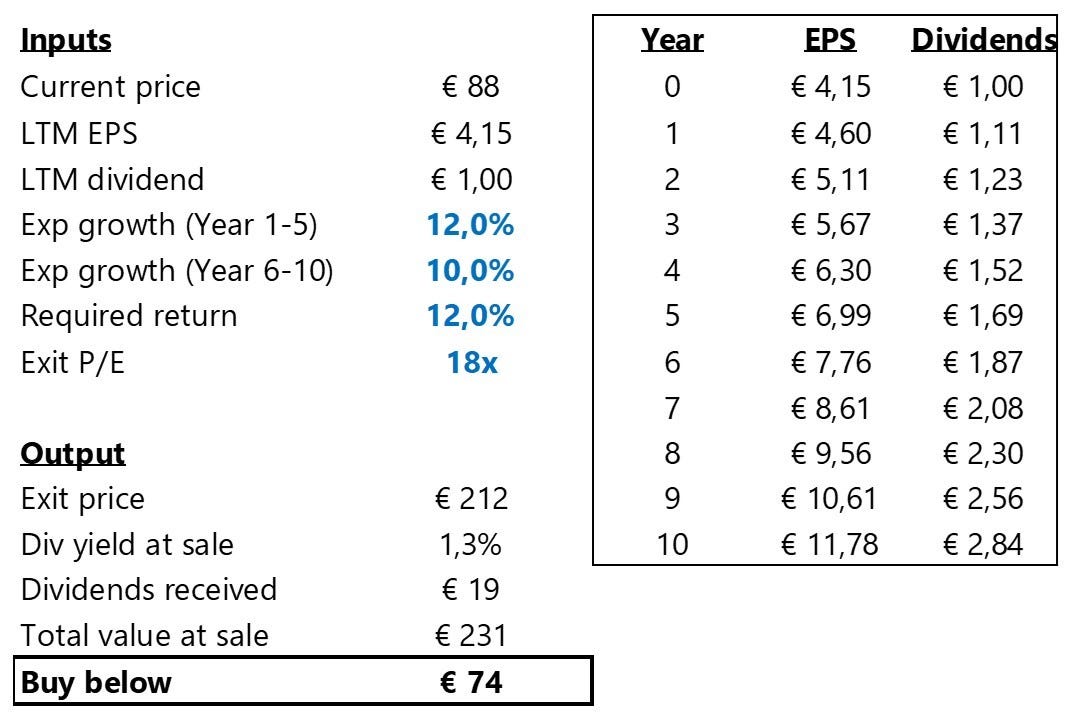

I have created a VERY SIMPLIFIED valuation model: assume:

Revenues and EPS growth in line with expectations for the market (12% for the first 5 years and 10% for the following 5): Reply has traditionally done better but I want to be conservative

Dividends also grow at the same rate, for a 25% payout

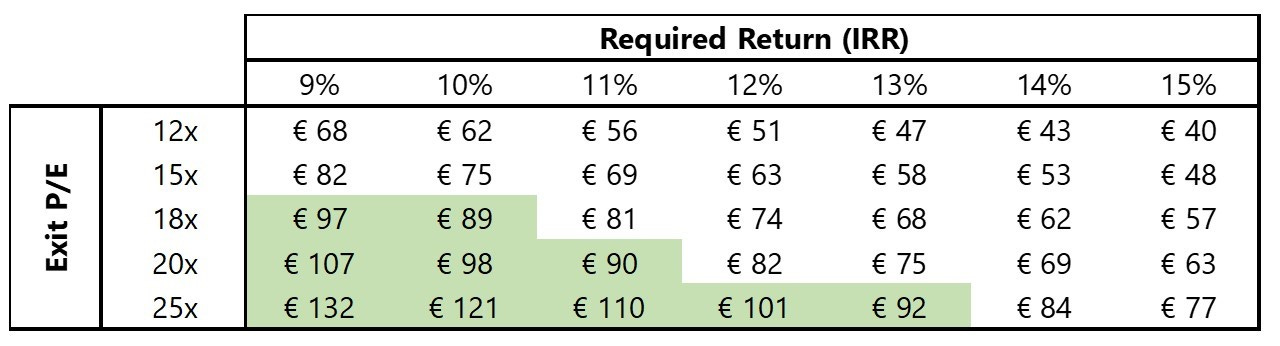

There is no multiple re-rating: in year 10 the exit P/E multiple is the same as the current valuation (18x)

To get a 12% IRR you should buy when price is €74, 16% below the current €88 price.

I’ve also run a sensitivity analysis on IRR and exit multiple (maintaining the same growth assumptions): with no re-rating, the current price implies an IRR of ~10%; if you aim for a 15% IRR you must count on higher exit multiples AND wait for a better entry price.

Conclusions

Reply is an innovative niche player, focused on high-growth areas (cloud computing, cybersecurity, artificial intelligence, IoT, …), whose demand will keep increase in the near future also thanks to the turning point in the digitalisation of business processes due to the pandemic. The digitalisation megatrend is resilient: many European countries are still well behind best practices in transitioning from traditional IT to era of digital, automated platforms.

As usual, it is useful to list the pluses and minuses of the company.

PROS

Not the biggest independent IT consultancy in Europe, but not a small start-up: brand recognition has improved a lot in the last 10 years

Strong track record of outperforming growth and margins

Founders still at the helm, bringing stability and long-term vision

Expertise in technological, core-business processes of clients

Strong, diversified client base in growth industries and increasing share of recurring revenues (customer retention and up-selling of other services)

No transformative deals difficult to digest and no empire building (size for the sake of size); the Head of M&A (Riccardo Lodigiani) has been with the company since 2000

Contrary to some competitors (Becthle, …), Reply avoid the sale of commoditised services (software/hardware) in all its distribution channels, even on behalf of third parties

CONS

Still very much dependent on Italy and, to a lesser extent, on Germany. (Actually, a nice problem to have as Italy is behind other countries in the digitisation process and the local business is still growing rapidly)

Reliance on acquisitions for growth: will they have to acquire bigger and bigger companies just to move the needle in terms of contribution to sales? Will they be forced to pay higher prices?

Relative dependence on top ten clients at around 35% of revenues (although per company’s policy none should be bigger than 10%)

A not insignificant amount of goodwill from acquisitions: this could be a problem should profitability go down

Not immune to soaring labour costs hitting the IT world, including a shortage of qualified employees and continued higher spending on training going forward, which could hurt margins

Increased competition from both large international players and smaller, innovative start-ups

IT budget cuts in the event of a cyclical downturn

Overall, I consider Reply’ quality as very good (probably not excellent: Accenture still has more brand recognition and business diversification). It was definitely overvalued in 2021 (P/E 45x, FCF yield less than 2%, hence the de-rating), and is probably fairly valued right now. My personal opinion is that going forward it should provide good returns, but mostly driven by growth in underlying fundamentals rather than another multiple re-rating: it could trade to a P/E of 22x or even 25x, but likely not again at over 40x.

I know: it’s a long, technical discussion full of flashy buzzwords, but this is how Reply presents its activities. Also, most of the charts in this section are from the Analysts Presentation from a couple of years ago: I do have a soft copy but I’ve not been able to locate it on the company’s website.

Admin functions (accounting, controlling, HR, …) are all centralised, but not sales: Reply places each managing partner (who are both product/technology and industry experts) at the forefront of acquiring projects and proposing original and specific solutions

Technically, there is a fourth segment, IoT Incubator (a portfolio of several start-ups, identified by Breed Reply), but its revenues are still zero

This is definitely not an exclusivity, all IT consultants partner with AWS, Google, Microsoft, …

An example is its relationship with FIAT as it transformed to FCA and now Stellantis, with Reply expanding its work from Italy to the rest of Europe and the US

Reply also takes part in international tenders: in December 2020, Machine Learning Reply (the group company specialising in Artificial Intelligence solutions) won the Airbus Quantum Computing Challenge (AQCC), a competition launched by Airbus in 2019 to address some of the major challenges in the aerospace industry by exploiting the computational capabilities offered by Quantum Computing

They are not interested in creating an empire: for example, Reply entered Romania only because both Vodafone and Unicredit asked to support their operations there

My very rough calculation: Reply paid €588 million since 2002 to add €366 million of inorganic revenues (see the financial numbers section for the background), so roughly 1.6x sales

The importance of brand is twofold: a) hiring a “famous” consultant is more expensive but also lowers the “reputational risk” for a project sponsor (“no one ever got fired for hiring McKinsey”, but they could be if they hired ABC Consulting and they screwed up); b) in order to get the best employees, you must have a good reputation with students, MBAs etc. (without good people you cannot charge high prices, so this is a self-reinforcing cycle)

I’ve excluded companies like Globant (which is more of software technology developer), DXC Technology (a vendor-independent IT services provider) and Visiativ (software solutions and development of Web platforms)

Also, add to the discussion the several acquisitions which mixes working capital with capex/intangibles in the cash flow statement

Accenture also acquired Objectivity (UK) in May but did not disclose the price

Great analysis! I also really liked the charts you shared from the analyst presentation. Coincidentally, I delved deep into Reply over the last three weeks too and recently shared my thoughts on the business.

There are a few things I noticed when I was reading annual reports of its competitors (such as Accenture, Cognizant, Infosys, Epam Systems):

- no comprehensive information about their top customers and revenue drivers from specific sectors, which makes it challenging to assess customer concentration

- lack of information about attrition levels, which I believe is very relevant for evaluating the operational performance and health

- no information available about the revenues from Reply's own platform solutions (any recurring revenues ?)

I'd love to hear your thoughts on these points. Thanks!

Why excluding Globant?