Bi-weekly recap #4

Intermediate Capital Group

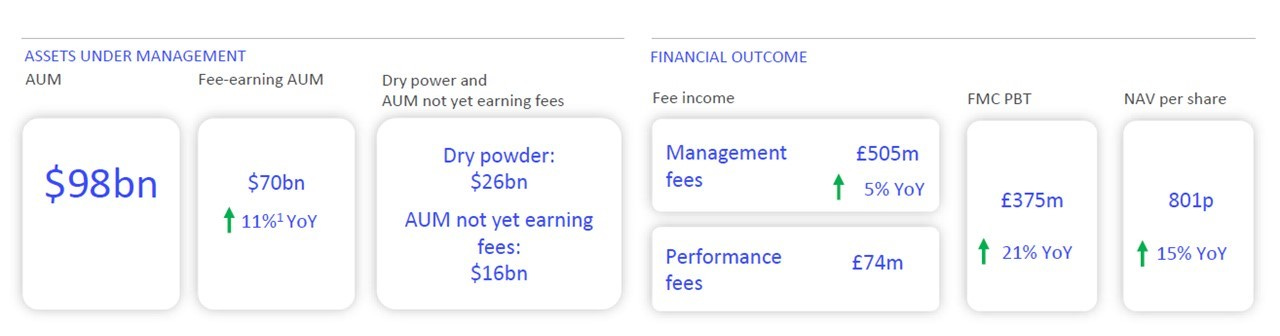

ICG had another banner year (FY end is March 2024): AUMs were up +22% to US$98bn, fee-earning AUM up +11% to US$98bn and management fees were above half a billion pounds for the first time ever (£505m). The growth over the last 5 years is impressive, +21% p.a. for both AUMs and management fees, and all this with actually increasing the weighted-average fee rate.

FY2024 was the second best ever fundraise period (US$13bn raised, US$7.7bn deployed and US$3.5bn realised), bringing the total for the last 3 years to an astounding US$46bn. ICG also scaled out it’s offering with the launch of a brand new LP secondaries fund, closed at a hard-cap of US$1bn (of which $50 million is ICG’s own capital) with 50% of the client base completely new to ICG.

Realisations were the only “sore” point, as the amount was lower than both the two previous years (US$6.4bn and US$5.3bn in FY2022 and FY2023, respectively), highlighting the widespread difficulties of private equity / credit of exiting investments.

Price has gone up a lot (+59% since the post last October and +29% YTD), and way above my estimate of intrinsic value (currently at £22 vs my estimates of £15-£17: today ICG trades at 9% mkt cap/AUM vs 6% at the time of the post), but the company is still executing flawlessly.

And no, I’m not going to say: “As long as the music is playing, you've got to get up and dance” (copyright: Chuck Prince)…

Ipsos

Ipsos’ numbers for 2023 were very much in line with what was expected: revenues slightly down (-0.6%, but better than what was implied in the first 9 months), but operating profits and core earnings both up (+0.5%).

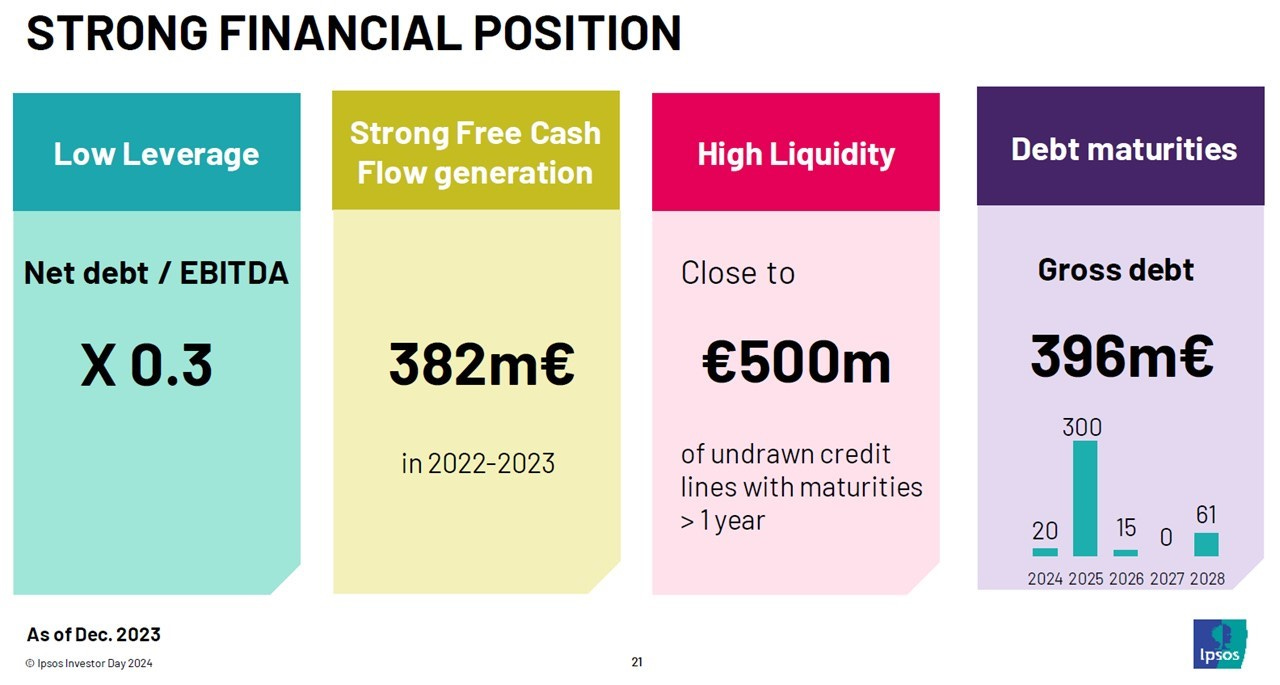

At the Investor Day in June the company reiterated the 2024 guidance (organic growth +4%, operating margin 13%) and the strong financial position: dividend for 2023 was also increased +22%.

The stock is up +14% since the post in December and +4% YTD (it was better before the -12% in June), and it never dipped below the €40 mark that I indicated as an even more attractive entry point for macroeconomic considerations (i.e. we enter into a soft recession). The considerations in the post are still valid, including the fact that Ipsos is the only publicly-listed pure market research company and might attract interest from private equity. While a bit more expensive than last year, it still trades at EV/EBIT 10x, P/E 12x with a ~7% FCF yield.

Big movers

Companies in the European SMID space with “big movements” (both up and down) during the month of June that are worth researching further: a lot of interesting French companies hurt by the current political uncertainty!

Interesting readings

Activist Investors Have a Simple Message for London Firms: List Elsewhere. Trian Fund Management recently amassed a stake in Rentokil, a UK-based pest control company. One of the activist's main calls to action is for the company to list in the US for better liquidity and access to a larger investor base.

“Founded in 2015, Zume's vision was quintessentially and hilariously Silicon Valley-esque in its scope: to utterly revolutionize the traditional pizza delivery model through cutting-edge robotics.” It didn’t work out exactly like that…